Break-Even Analysis for Manufacturing Business: Formula, Examples & What Every MSME Founder Must Know

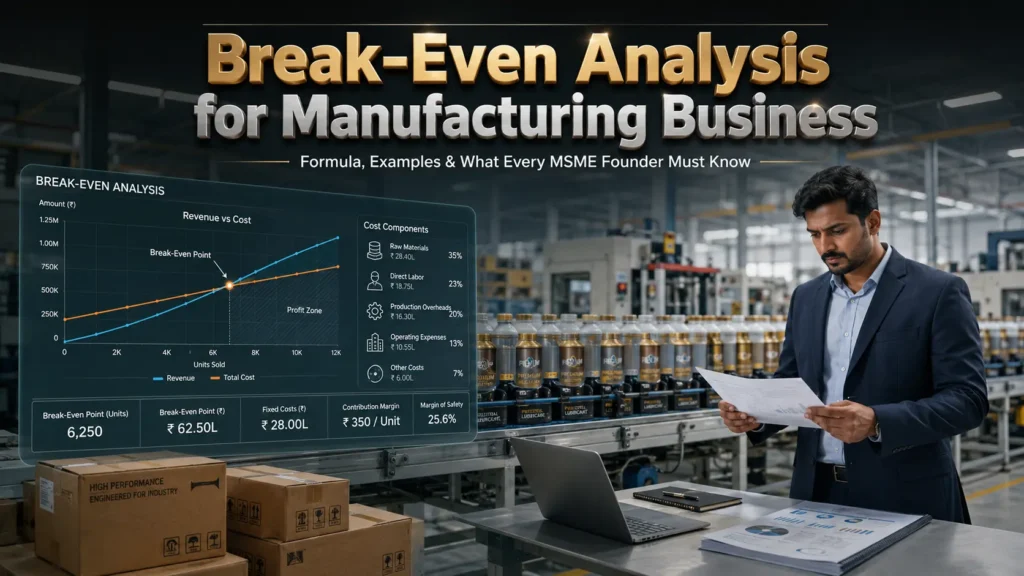

Break Even Analysis for Manufacturing Business The Number That Decides Everything — Before You Sell a Single Unit Only 72% of the first-generation manufacturing entrepreneurs in India have never worked out the break-even point before they go into production. This number is not only a number; it is a figure from a SIDBI MSME Pulse report. It is a confession. It is like driving on the Yamuna Expressway with your headlights off — fast, confident and headed for a crash. What is so deadly about this number when left unchecked; you can be operating at 80% capacity with a salary of ₹8 lakh per month and still be in the red. This is a common occurrence in industrial belts ranging from Morbi to Meerut every day. The machine is running. Workers are paid. Orders are flowing. However, the unit is running a leak! Break-even analysis will tell you precisely how many units you need to produce (or how much revenue you need to clock in) before your business starts to break even and begin to turn a profit. It is NOT a Finance Department Tool! It serves as a survival tool. It is a must-know for every MSME owner, entrepreneur with a startup investment of ₹20 lakh or ₹2 crore. In this article, you will get the formula, real-world examples in India, and the step-by-step process to compute your break-even – for any product or production scale! Why Most MSME Units Price Blind — and Pay for It According to the government, India has more than 63 million MSMEs, accounting for a whopping 30% of the country’s GDP and 45% of its exports. According to the Annual Report of the Ministry of MSME, there are more than 63 million MSMEs in India which contribute to almost 30% of GDP and 45% of exports in the country. Among these are about 14 million manufacturing units. However, there is an enduring problem in this sector – most of the owner’s price on the gut rather than on a cost basis system. The problem is structural. In clusters such as Ludhiana (hosiery), Rajkot (engineering goods), Firozabad (glassware) and Sivakasi (fireworks and matches), the pricing for first generation entrepreneurs is passed on from the older ones. They use their lower prices to compete and don’t know if those competitor prices are profitable at all. The outcome: narrow profit margins that always disappear when costs of input increase. Data from the Confederation of Indian Industry (CII) and the National Sample Survey Office (NSSO) reveals that more than 50 per cent of manufacturing units in India that close are not due to lack of demand but due to mismanagement of cash flows – a lot of which is directly related to under-pricing and unmanaged fixed-cost overhead. The three industrial towns of tier-2 and tier-3, namely, Hapur in Uttar Pradesh (rubber goods), Morbi in Gujarat (ceramics) and Batala in Punjab (agricultural equipment) are most vulnerable to this issue. In each of these clusters, new firms regularly enter without considering break-even analysis — for prices that just cover variable costs and exclude fixed costs. The immediate result: They ran straight into a wall at 6–18 months of service. Not because the market was against them. As the numbers were never calculated. Related Article: 100 Industrial Parks Worth ₹33,660 Cr: Top Business Ideas for MSME Founders Table 1: Break-Even Analysis Snapshot — Indian Manufacturing Sectors Industry / Product Fixed Costs/Month (₹) Variable Cost/Unit (₹) Selling Price/Unit (₹) Break-Even Units/Month Garment Unit (Tiruppur, TN) 3,20,000 180 320 2,286 Plastic Moulding (Rajkot, GJ) 4,80,000 42 95 906 Namkeen / Snack Food (Indore, MP) 2,10,000 28 55 7,778 Steel Fabrication (Ludhiana, PB) 6,50,000 220 440 2,955 Agarbatti / Incense (Bengaluru, KA) 1,20,000 12 28 7,500 Paper Cup Manufacturing (Pune, MH) 3,80,000 0.35 0.75 9,50,000 cups Source: Illustrative estimates based on MSME cluster data from SIDBI, CII, and industry association benchmarks. Actual figures vary by state and scale. The Formula — Simple, Powerful, Non-Negotiable There is one basic equation to break-even analysis. All other are modifications of it. Break-Even Point (Units) = Fixed Costs ÷ (Selling Price per Unit − Variable Cost per Unit) The Contribution Margin in this formula is the denominator or Selling Price per Unit minus Variable Cost per Unit. It indicates the amount of each unit sold that covers your fixed costs and ultimately, your profits. A revenue-based version is also available: Break-Even Point (Revenue) = Fixed Costs ÷ Contribution Margin Ratio As selling price increases, the contribution margin ratio has the same trend as the contribution margin.As the selling price goes up, the contribution margin ratio follows the same pattern as the contribution margin. Worked Example: Plastic Moulding Unit, Rajkot A first-generation businessman establishes a plastic injection moulding shop in Rajkot. The data from Gujarat Industrial Development Corporation (GIDC) suggests that the rent of a standard GIDC shed of 1500 sq ft in Metoda Industrial Estate is in the range of ₹35,000 to ₹45,000 per month. He has fixed monthly expenses of the following amounts: Factory shed rent (GIDC Metoda): ₹40,000 Loan EMI on machinery (₹18 lakh @ 10.5% over 5 years): ₹38,500 DGVCL (Electricity fixed charges): ₹22,000 Salaries — supervisor + admin: ₹55,000 Depreciation, insurance, misc: ₹24,500 Total Fixed Costs: ₹1,80,000 per month He incurs the following variable costs per kg of moulded output: raw material (HDPE) ₹92, direct labour ₹18, power per unit run ₹12 and packaging ₹8. He sells the product to a distributor at a price of ₹185 per kg. Contribution Margin = ₹185 − ₹130 = ₹55 per kg Break-Even = ₹1,80,000 ÷ ₹55 = 3,273 kg per month The monthly sales in this unit have to be 3,273 kg to be profitable. At 5,000 kg — a realistic 70% capacity run — it earns ₹94,985 in monthly profit. At 60% (4,300 kg), profit is ₹56,650. The numbers shouldn’t tell the originator what to shoot! Why Government Schemes Must Factor into Your Break-Even PMEGP (Prime Minister’s Employment Generation Programme) scheme provides capital