Techno Economic Feasibility Report for Bank Loan

Contents

- 0.1 The Rejection That Wasn’t About the Business

- 0.2 Related Article: Detailed Project Report (DPR) Consultants in India: How to Get Bank Loan and Government Subsidy for Your Business

- 1 Why Most Project Reports Fail at the Bank Counter

- 2 Table 1: Common TEFR Deficiencies and Their Impact on Loan Applications

- 3 The Window That Policy Has Opened

- 4 Table 2: Key Government Schemes That Require a TEFR / DPR for Sanction

- 5 How to Build a Bank-Grade TEFR, Section by Section

- 5.1 1 — Executive Summary (4–6 pages)

- 5.2 2 — Promoter Background and Business Plan (8–12 pages)

- 5.3 3 — Product and Market Analysis (15–20 pages)

- 5.4 Get Detailed Project Report (DPR): Project Reports & Profiles

- 5.5 4 — Technical Feasibility (20–30 pages)

- 5.6 5 — Statutory Approvals and Licences Required

- 5.7 6 — Financial Projections (25–35 pages)

- 5.8 Turn your budget into a successful business plan

- 6 Table 3: Investment Breakdown for Preparing a TEFR — Cost and Timeline Guide

- 7 What a Good TEFR Costs vs. What a Bad One Costs You

- 8 Entrepreneur Spotlight

- 9 Where to Get Expert TEFR Assistance

- 10 The One Thing to Do Before Your Next Bank Meeting

- 11 Frequently Asked Questions

The Rejection That Wasn’t About the Business

In India, about 70% of MSME loan applications may be rejected not due to the strength of the business idea but because of the project documents. That number, often quoted in the Reserve Bank of India’s financial inclusion reports, is an unfortunate paradox – India has the capital, and the ideas are brought to the table by the nation’s entrepreneurs, but the paperwork doesn’t.

Techno-Economic Feasibility Report (TEFR) is the document that forms the basis of all possible bank sanction processes. If you ask any MSME relationship manager from Punjab National Bank, Bank of Baroda or SIDBI, they will all reply the same: MSME feasibility report. It’s not about the entrepreneur’s enthusiasm. Not the opportunity pitch for the market. The report.

In India, most first-generation entrepreneurs, who are rice mill owners in the state of Chhattisgarh, garment manufacturing in Tiruppur, cold storage investor in Agra, etc., take months to choose the equipment and negotiate land, and invest just two days in the report. That’s the exact opposite ratio. Poorly written TEFR will sink an otherwise good project. With a proper structure a one can sanction a ₹5 crore in 8 weeks.

Here’s the inside scoop on what a bank-grade TEFR includes, how to assemble each section, and what sets it apart from the rejected documents that languish in a credit manager’s rejection bin.

Related Article: Detailed Project Report (DPR) Consultants in India: How to Get Bank Loan and Government Subsidy for Your Business

Why Most Project Reports Fail at the Bank Counter

The formal banking system consisting of public sector banks, private banks and development finance institutions (DFIs) such as SIDBI have together allocated more than ₹22 lakh crore to support MSME loans as per their respective priority sector policies. However, penetration of credit into micro and small businesses is still very low. The shortage is not due to the lack of money. It is caused by poor quality project documentation.

One of the most consistent findings in the Reserve Bank of India’s annual report on MSMEs is that ‘inadequate financial data’ and ‘insufficient technical details’ are the main reasons for the MSME applications to be rejected. There are many applicants that present what they term a ‘project report’ which is actually a simple spreadsheet with projected revenues and a quotation from a supplier pasted into it.

A structured document which contains three layers of analysis is called a Techno-Economic Feasibility Report:

- Analysis of the technical aspects — what is to be produced, how it is to be produced, and what infrastructure is required for the production.

- Economic analysis — will the unit be able to produce cash sufficient to pay back the loan and to show a profit?

- Risk evaluation – what can go wrong and have they done something to minimise the risk?

The TEFR is used by banks in India as a report for Due Diligence Input Report (DDIR) before the credit sanction committee meeting. The credit officer has nothing to go on but the entrepreneur’s past, if there is a credible TEFR.

As per the Ministry of MSME’s Udyam registration portal, there are more than 4.6 crore MSME’s in India registered with the ministry. Only a small proportion of these have sought formal bank finance. One of the reasons is the quality of documentation – which is 100% fixable.

Table 1: Common TEFR Deficiencies and Their Impact on Loan Applications

| TEFR Deficiency | Section Affected | Bank’s Concern | Rejection Risk |

| No break-even analysis | Financial Projections | Can the unit survive a bad quarter? | High |

| Missing pollution NOC reference | Regulatory Compliance | Will the plant face shutdown orders? | High |

| Equipment cost without quotations | Capital Cost Estimate | Is the capex realistic or inflated? | Medium-High |

| No raw material sourcing plan | Technical Feasibility | Supply disruption risk unquantified | Medium |

| Promoter contribution not shown | Funding Pattern | Is the promoter committed? | High |

| No sensitivity analysis | Risk Assessment | What if revenue falls 20%? | Medium |

| Generic market study, no India data | Market Feasibility | Is there real demand for this product? | Medium-High |

| Missing working capital estimate | Financial Projections | How will day-to-day operations run? | High |

The Window That Policy Has Opened

The credit scenario for MSMEs manufacturing has significantly improved in India. There are now several policy instruments that reduce the risk on bank lending to units that provide a credible feasibility plan.

Collateral free loan guarantees up to ₹5 crore have been introduced for micro and small enterprises through the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) run by Government of India and SIDBI. Banks are much more likely to make loans through CGTMSE — and a decent TEFR is the most important document needed to activate the guarantee.

PMEGP (Prime Minister’s Employment Generation Programme) is administered by KVIC, which provides capital subsidy ranging from 15% to 35% of the project cost for the first-generation entrepreneurs for the setting up of manufacturing units. Subsidy shall be disbursed based on the Detailed Project Report (DPR) – which is equivalent to a TEFR.

Production Linked Incentive (PLI) schemes in 14 sectors (food processing, specialty chemicals, electronics, etc.) mandate for larger investments demand techno-economic documents to be submitted when claiming incentives. Some states such as Gujarat, Tamil Nadu, Karnataka and Telangana have state-level MSME investment policies which require a feasibility report for disbursement of incentives.

Having a well-balanced TEFR is more than just a business case for bank loans. A well-formulated report is also a:

- Rationale for the application of CGTMSE guarantee

- Requests for refinancing by SIDBI will be handled technically by the technical input

- The main exhibit in an equity investment or joint venture talks

- The compliance documents required for availing the MSME incentive from the state governments.

According to SIDBI’s MSME Pulse report, credit is available at lower interest rates and with faster sanctioning periods at MSMEs with structured techno-economic documentation (6–10 weeks) as compared to the undocumented ones (18–24 weeks).

Get Detailed Insights from This Book: Select & Start Your Own Industry

Table 2: Key Government Schemes That Require a TEFR / DPR for Sanction

| Scheme | Administered By | Benefit | TEFR / DPR Requirement | Applicable Sectors |

| PMEGP | KVIC / State DIC | 15–35% capital subsidy | Mandatory DPR submission | All manufacturing |

| CGTMSE | SIDBI + GoI | Collateral-free guarantee up to ₹5 Cr | Technical-financial feasibility required | Micro & Small units |

| MUDRA (Tarun) | Scheduled Banks | Loan ₹10 lakh – ₹20 lakh | Basic project report needed | All micro enterprises |

| SFURTI | Ministry of MSME | Common facility centre funding | DPR with equipment list mandatory | Khadi, village industries |

| PLI Schemes | Sector Ministries | Production-linked incentive 4–20% | Techno-economic doc for claims | 14 specified sectors |

| Stand-Up India | SIDBI / Banks | ₹10 lakh – ₹1 Cr for SC/ST/Women | Detailed project report required | Greenfield manufacturing |

| State MSME Policy | State Industries Depts | Capital/interest subsidies | Feasibility report for disbursement | State-specific sectors |

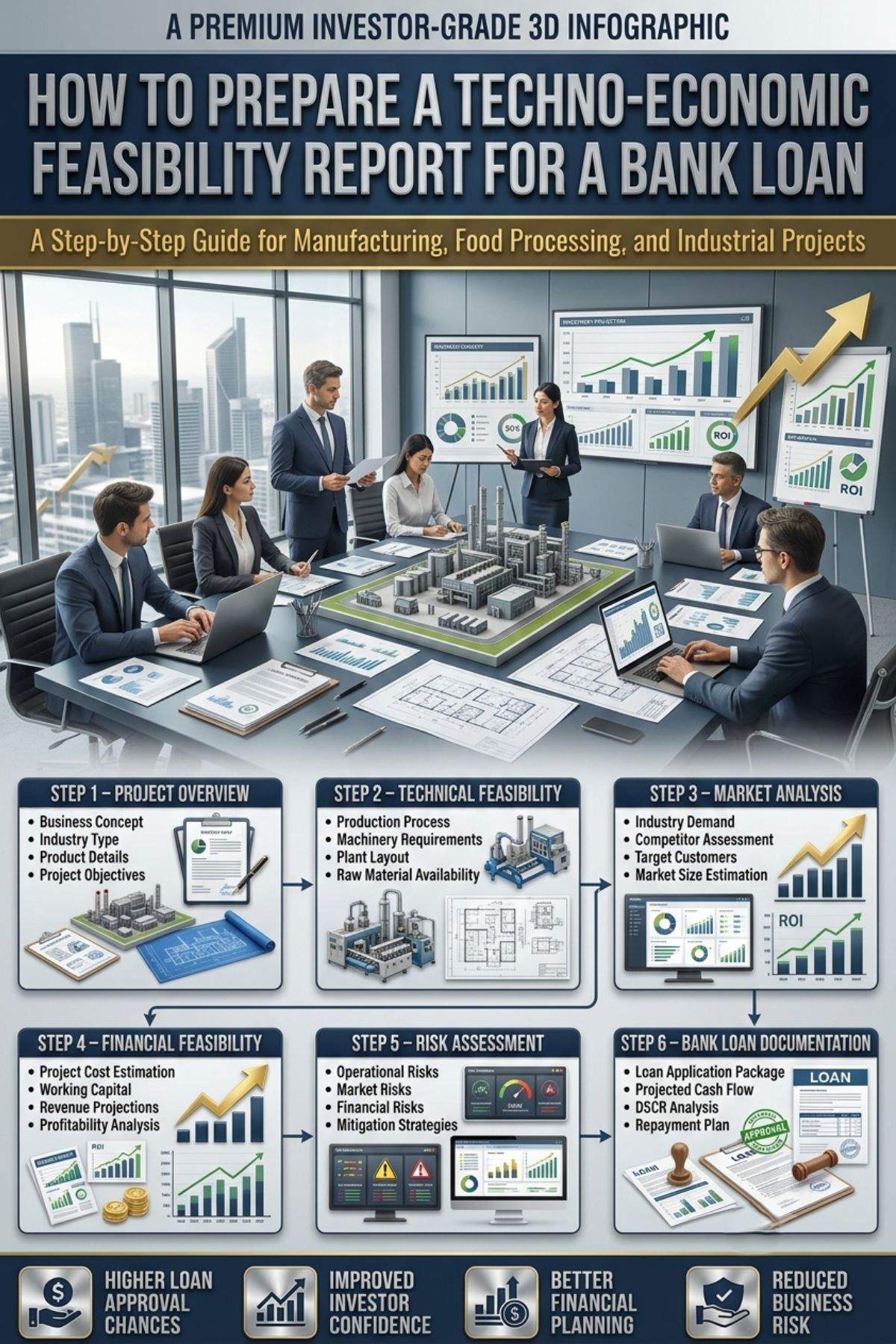

How to Build a Bank-Grade TEFR, Section by Section

The length of the complete T.E.F. Report for an Indian bank loan is approximately 80–150 pages. Each of the following sections must include the following information, and why banks care about it.

1 — Executive Summary (4–6 pages)

It is the part that credit managers will read first, and only. It is required to include: Name of the promoter and entity, the proposed product, the location, total project cost, proposed funding pattern (debt: equity ratio), expected revenue when at full capacity, Net margin and the Payback period. Keep it factual. If the credit officer makes one mistake, such as a debt: equity ratio that does not agree with the projected financial statements, then he won’t read page two.

2 — Promoter Background and Business Plan (8–12 pages)

Banks lend to people, not projects. Put their biography, qualifications, past experience, and maybe most of all, their net worth statement. There needs to be a formal statement of net worth (certified by a CA). Provide the three most recent Income Tax Returns (ITRs) for existing promoters. If you are a first-generation entrepreneur who has none business experience, an employment history and vocational training certificates are fine.

3 — Product and Market Analysis (15–20 pages)

The section needs to address three questions: Does there have to be a market for this product? How big is it in India? What is the realistic penetration in the market this unit can achieve? Utilize statistics from Government sources (such as Annual Survey of Industries (ASI), DPIIT, NSSO or industry-specific organisations such as CPCB, FSSAI, AEPC or BIS). Steer clear of general global market reports. A bank credit officer in Ludhiana is not interested in demand in Southeast Asia, rather he wants to know what the demand is in Punjab and the neighbouring states.

The data available on the Annual Survey of Industries (ASI) from the Ministry of Statistics is a great primary source for the production volumes, input costs and profitability benchmarks of various sectors in the Indian states.

Get Detailed Project Report (DPR): Project Reports & Profiles

4 — Technical Feasibility (20–30 pages)

This is the nitty-gritty of engineering in the report. It must cover:

- Describe the manufacturing process and draw a process flow diagram.

- The assumptions of installed capacity and actual utilisation (usually 60% in Year 1, 80% in Year 3)

- A layout plan for land and buildings. A layout plan of land and buildings.

- Machinery and equipment specifications with details of types, makes and supplier quotes

- Both power (kVA load) and water (KLD) consumption rates are included. Power (kVA load) and water (KLD) consumption rates are included.

- Identification of raw materials, their states of supply and indicative price per tonne or unit

- Quality control systems and required certifications (BIS, FSSAI, ISO, etc.)

All the numbers in this section should be supported by a quote, a government notification, or a published source. Banks will not believe ‘estimated at market rates’ unless accompanied by supporting data.

5 — Statutory Approvals and Licences Required

Break down all the approvals that must be obtained for the industry in question, and arrange them in a timeline. Typical approvals for Manufacture of MSMEs are:

- Online Udyam Registration – Free, immediate and easy at udyamregistration.gov.in

- GST Registration — It is compulsory for the units having turnover exceeding ₹40 lakh.

- A state labour department grant of a factory license under the Factories Act.

- This is a State PCB Pollution Control NOC (Consent to Establish, Consent to Operate).The State PCB Pollution Control NOC (Consent to Establish, Consent to Operate) is this.

- Quality checks for halls — Bureau of Indian Standards (BIS) certification, as applicable

- The Food Safety and Standards Authority (FSSAI) is responsible for issuing a license for food/agro processing units.

- Local Municipal Body / Fire Department (LMB/FD)

- The project involves installing a 220-volt power connection, including obtaining a load sanction from the State DISCOM.

6 — Financial Projections (25–35 pages)

It’s the most closely analysed part of the bank. It must contain:

- Total project cost statement (capital expenditure + pre-operative expenses + working capital)

- Funding statement of finances with details of debt, equity and subsidy.

- This presentation brings the expected profit and loss account for 5–7 years to a focus.

- A projected balance sheet for 5-7 years. A 5–7-year projected balance sheet.

- Cash Flow Statement (including the calculation of DSCR)

- Break-even point analysis (BEP in units and in INR)

- The number of times your debts are covered by cash flow.A bank’s preferred minimum Debt Service Coverage Ratio (DSCR) is 1.3:1.

- Internal Rate of Return (IRR) and Net Present Value (NPV)

- Sensitivity analysis demonstrating results on IRR if revenue drops 10 – 20% or costs increase 10 – 20%

The number that is the most important in the financial section is the DSCR. If the DSCR is consistently high throughout the repayment period, it will speed up the sanction. If it’s less than 1.25:1, it will trigger queries, and less than 1:1 it will be rejected.

Turn your budget into a successful business plan

Table 3: Investment Breakdown for Preparing a TEFR — Cost and Timeline Guide

| TEFR Component | Preparation Method | Estimated Time | Estimated Cost (INR) | Key Data Source |

| Executive Summary | In-house or consultant | 2–3 days | Included in overall | Promoter documents |

| Market Analysis | Industry consultant | 7–10 days | ₹15,000–₹40,000 | ASI, DPIIT, NSSO data |

| Technical Feasibility | Industry + engineering consultant | 10–15 days | ₹25,000–₹60,000 | Supplier quotations, PCB norms |

| Financial Projections | CA / financial consultant | 5–7 days | ₹20,000–₹50,000 | Bank norms, RBI guidelines |

| Regulatory Compliance | Legal / compliance consultant | 3–5 days | ₹10,000–₹25,000 | State govt portals |

| Full TEFR from NPCS / DPR firm | Specialised consultancy | 21–30 days | ₹35,000–₹1,50,000 | Proprietary DPR database |

| Chartered Accountant Certification | CA firm | 3–5 days | ₹10,000–₹30,000 | Audited financials / projections |

What a Good TEFR Costs vs. What a Bad One Costs You

The cost calculations for preparing a TEFR are simple. The cost of a professionally prepared Techno-Economic Feasibility Report for a project between ₹35000 – ₹150000 depends on the complexity of the sector, depth of financial modelling and the need for a field visit.

That leaves a documentation cost at 0.35–1.5% of the loan amount on the books, against the loan sanction of ₹1 crore. A TEFR cost is almost negligible compared to the cost of rejection that will cost you 12-18 months for your plant to be commissioned.

To help you understand what to expect when planning a project, here are realistic estimates of TEFR costs based on project size:

- Micro project (₹10–25 lakh): TEFR cost ₹20,000–₹40,000, preparation time 15–20 days

- Small project (₹25 lakh – ₹2 crore): TEFR cost ₹50,000–₹80,000, preparation time 20–30 days

- Medium project (₹2–10 crore): TEFR cost ₹80,000–₹1,50,000, preparation time 25–35 days

- Large MSME project (₹10–50 crore): TEFR cost ₹1,50,000–₹4,00,000, preparation time 35–60 days

The financial benefit: If a well-structured TEFR is agreed with the bank with DSCR 1.5:1 or above and a sound market analysis, you can avail of a benefit in the form of a reduction in interest spread by 0.25–0.5%. On a loan of ₹2 crore with interest at 9% for 7 years, it translates to a saving of ₹2.5–5 lakh in interest costs. The document proves its worth before you sign the sanction letter.

Financial ratios can be compared with the financial ratios of MSMEs from the SIDBI’s MSME sector profiles and the Reserve Bank of India’s data on sectoral credit flow to MSMEs.

Entrepreneur Spotlight

Manoj Tiwari | Raipur, Chhattisgarh

Manoj is operating a medium scale rice processing unit and took a term loan of ₹1.2 crore under PMEGP. With the first application, his bank asked for a project report which was missing a break-even analysis and pollution NOC reference. He issued a proper TEFR to NPCS and got it back within 6 weeks and was fully sanctioned. Now, his group is earning ₹2.8 crore per annum with 75 percent production at the plant. The lesson: Banks don’t turn down good businesses; they turn down incomplete paperwork. Ensure that the techno-economic report is correct first time.

Where to Get Expert TEFR Assistance

Niir Project Consultancy Services (NPCS) is one of the premier industrial consultancy firms of India with more than 45 years of experience in preparing Techno-Economic Feasibility Report and Detailed Project Report (DPR) in 50+ industry sectors for entrepreneurs. NPCS is based in New Delhi and develops project reports, which are bank ready and include all mandatory sections: technical feasibility, financial projections (including DSCR and IRR calculation), market analysis (including India specific data), regulatory approvals mapping and plant layout designs.

Their database at niir.org contains more than 8,000 project reports across a wide range of manufacturing sectors including agro-processing, chemicals, textiles, pharmaceuticals, plastics, construction materials and more. NPCS is also active for entrepreneurs who require ready reference reports as well as customized preparation of TEFR.

A resource platform to help MSME entrepreneurs make sound investment, licensing, and project planning decisions: entrepreneurindia.co

NPCS reports are accepted as reliable inputs by public sector banks, SIDBI, state finance corporations and the application committees of CGTMSE. The company is ISO 9001:2015 certified and accredited by D-U-N-S.

The One Thing to Do Before Your Next Bank Meeting

Don’t take the project report lightly. Don’t think about making the TEFR only if your bank requests it; think about creating the TEFR to make your bank want to extend you money. Every rupee you save by foregoing a professional report could set you back months and the optimum working window of your project.

This is what you should do this week: Determine which scheme the project can avail of – PMEGP, CGTMSE, PLI, or State Level MSME incentive. Go to the government portal to download the DPR format of that scheme. In this case, if the DPR structure is more complex than what you can do on your own, hire a specialist consultancy such as NPCS for the preparation of the DPR in 3 to 4 weeks.

Credit window is open. The schemes are financed. The only thing that remains is if your paper work is good enough to get through the door.

Frequently Asked Questions

Q1: What is the expense of applying for a TEFR for a bank loan in India?

The cost of a professionally prepared TEFR by a reputable consultancy firm range from ₹35,000 to ₹1,50,000, depending on the size of the project, the complexity of the sector, and the need for field visits. Basic DPRs can be obtained for micro projects of up to ₹25 lakh at ₹20,000–₹40,000. This is such a small cost of the loan amount and almost always gets repaid because of quicker sanction and improved interest rates.

Q2: Which licenses do I have to add to the TEFR for a manufacturing unit?

Mandatory Licences vary from sector to sector, however, Basic requirements for most manufacturing MSMEs are as follows: Udyam Registration, GST, Factory Licence (State Labour Dept), Pollution Control NOC (State PCB), and Fire NOC. Food or agro-processing units also require FSSAI license. Additional clearances are required for chemical/pharmaceutical units from the Drugs Controller or Petroleum and Explosives Safety Organisation (PESO). In the TEFR, provide a complete set of all the required approvals along with anticipated timelines.

Q3: What is a DSCR, and why is it important for banks?

Debt Service Coverage Ratio (DSCR) is a term used in finance. This is calculated as the ratio of a unit’s annual net cash accrual to the annual cash repayment requirement (principal + interest) for loans. The minimum DSCR ratio required by most public sector banks is in between 1.25:1 and 1.50:1. The DSCR of 1.75:1 or higher greatly expedites the sanction process. If your financial forecast indicates that DSCR is less than 1.25:1, adjust the debt: equity ratio or the repayment period before presenting your financial forecast.

Q4: Can I create the TEFR myself or do I need to hire a consultant to do it for me?

No law or regulation mandates that a consultant be used. Self-prepared TEFRs, on the other hand, are more likely to be returned with questions due to a lack of financial modelling, sensitivity analysis, or references to regulations. If you are a finance or engineering professional, you can write a section on your own — but before you submit any report, always ensure that the financial projections are certified by a CA and that the report is formatted as per the guidelines set out by the relevant bank or scheme DPR.

Q5: What are the best Government schemes for the Manufacturing MSME loans?

Collateral free loans of up to ₹5 crore are the most important scheme for first generation entrepreneurs as it is the most common hurdle faced by them when it comes to getting loans. The capital subsidy given under PMEGP for the manufacturing units is direct subsidy of 15-35%. The working capital loan amount up to ₹20 lakh is covered by MUDRA loans. Check out all the active schemes on the Ministry of MSME portal.

Q6: How does NPCS help in the preparation of TEFR?

NIIR Project Consultancy Services (NPCS) provide Detailed Project Reports and Techno-Economic Feasibility Reports for manufacturing units in all the MSME sectors. They create technical specifications, financial projections with DSCR and IRR, analysis of the market with Indian data, plant layout design and maps for regulatory approval. Reports can be found as ready-reference documents, or as a prepared report for a particular project. Visit niir.org or

For more information visit entrepreneurindia.co.