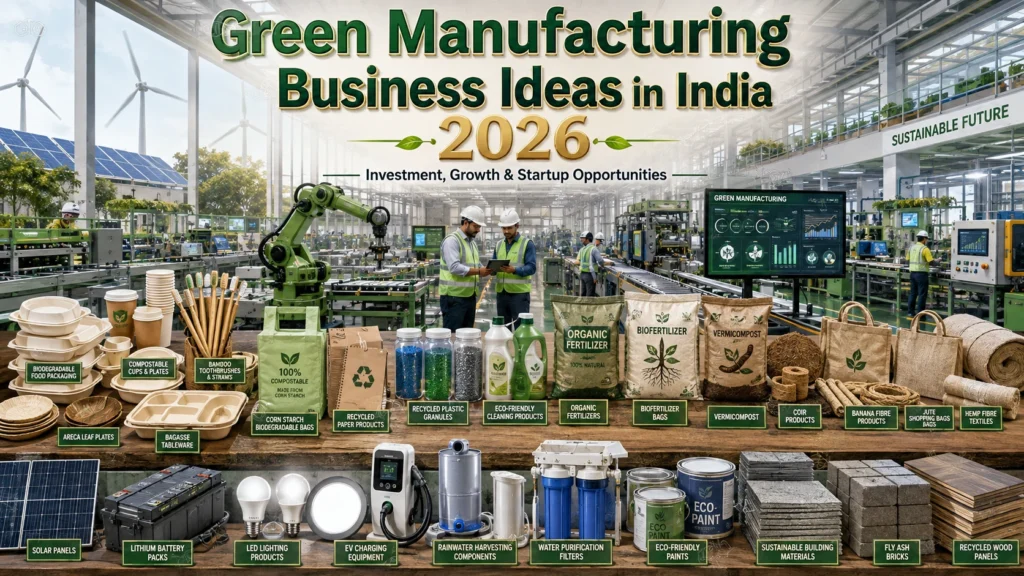

Green Manufacturing Business Ideas in India for 2026

Opportunities for Circular Economy, Recycling and Eco-Friendly Products that are Profitable. The concept of sustainability has grown from being a catch phrase into a viable business model. With India taking a step toward a circular economy, recycling and eco-friendly manufacturing have become regulated, financeable, and future-proof industries. This is a once-in-a-lifetime opportunity for entrepreneurs looking for new and innovative green manufacturing business ideas in India for 2026. There are several trends pushing demand toward sustainable products, including tighter plastic bags, longer producer responsibility regulations, and green-financing incentives. The purpose of this guide is to highlight the most viable manufacturing concepts that are green and circular economy that can be pitched to startups, MSMEs and investors. Where they are successful, they have both a positive environmental benefit and a strong economic return, and many have a steady source of raw materials because they are a waste stream others are willing to pay for. Size of investment is no restriction; it is the process know-how and compliance that is important. In addition, you’ll get practical advice on licensing, government assistance, and how to take your idea from concept to product throughout. The agricultural residue, e-waste, used batteries and plastic waste that India produces annually is immense and a significant proportion of which is unutilised. Every waste stream is a raw material opportunity to a green manufacturer. Meanwhile, extended producer responsibility regulations are making brands responsible for recycling and sustainable packaging, meanwhile, which offers an assured market for conforming units. Thus, it is that green manufacturing is structurally attractive in 2026, being cheap inputs and mandated demand. Related Article: The Green Manufacturing Revolution: Paper Water Bottles, Bioplastics & Biodegradable Products Why Green Manufacturing Is Booming in India The move towards a circular economic system in India has taken recycling to an increased degree of regulation, bringing it to an industry level with long-term demand. The E-waste, battery waste and plastic reprocessing now have the regulatory certainty that provides a consistent flow of raw materials and access to green financing. Meanwhile, there is an increasing consumer demand for biodegradable and compostable products from global brands and Indian consumers which creates export avenues for eco-friendly products. Green manufacturing’s strategic value is “waste to value economics”. If your raw material is agricultural residue, old electronics or used batteries, your margins will be low, your environmental branding will be high, and you’ve got a powerful combination. Top Green Manufacturing Business Ideas in India for 2026 1. E-Waste Recycling and Metal Recovery In India, electronic waste recycling has been now legally regulated and has made the raw material available to the electronics recycling units and also created a steady demand for the recycling industry. Dematerializing copper, gold, aluminium and reusable parts from waste e-waste is a viable, eco-friendly, economically valuable scalable business. Only a tiny percentage of e-waste is processed in India and there is a huge gap in between of the organised recyclers. Building a regulated e-waste recycling centre complete with the required pollution-control and extended producer responsibility authorisations is the professional way to begin a business to securely and reliable provide this service to companies that are legally required to recycle their own products. 2. Lithium-Ion Battery Recycling As automotive and consumer electronic batteries end their service, the extraction of high-value minerals like nickel, lithium and cobalt presents an eco-friendly and economic choice. Battery recycling truly is one of the new manufacturing frontiers in India for 2026, supported by policy, and increased volumes. With India importing close to 100% of these critical minerals, it is essential that there is a strategic interest in their recovery in addition to being profitable, and cell manufacturers are more willing to purchase recovered minerals to mitigate their import risk. The first to learn the chemistry to recover the materials and to be able to obtain a regular stream of spent batteries will be able to establish a position which will serve them for decades. Read the Complete Book Here: Handbook on Lithium-Ion & Lead-Acid Battery Production and Recycling 3. PLA Bioplastic and Biodegradable Cutlery Manufacturing Poly Lactic Acid (PLA) is a biodegradable plastic, the world’s fastest growing, made from renewable corn starch. As single-use plastic restrictions increase, there is a great opportunity for restaurants, caterers and cloud kitchens to brand their cutlery, plates and packaging with PLA, a material that’s being manufactured for export. 4. Biochar Production from Agricultural Waste Biochar tackles both agricultural productivity and waste management by turning crop residue into a soil amendment and water filtration material. Crop residue is utilized as biomass in millions of tonnes every year in India which leads to air pollution; hence the conversion of this residue into a useful product has both commercial and environmental benefits. Biochar is a low barrier, high relevance, green manufacturing concept with relatively low start-up costs and increasing market relevance in the field of sustainable and organic agriculture, which is particularly suitable for bioentrepreneurs in rural regions who are close to agricultural clusters. 5. Sustainable and Biodegradable Packaging Sustainable packaging is on the rise as companies move away from plastic packaging and towards biodegradable options in response to legislation and consumer demand. The applications for bagasse tableware, moulded-fibre packaging and compostable films are of huge and increasing importance for restaurants, food delivery, airlines and e-commerce. Biodegradable packaging benefits from government incentives and increased consumer demand as single-use plastics are increasingly subject to regulation and large buyers are increasingly adopting and requiring sustainability objectives, making it one of the most bankable sustainable manufacturing ideas for 2026. Get Detailed Project Report (DPR): Biodegradable Packaging & Bio-based Polymers Guide 6. Plastic Reprocessing and Recycled Granules Plastic reprocessing units convert post-consumer and industrial plastic waste into plastic granules which are used to make plastic product. This business is now subject to the extended producer responsibility norms that guarantee it a consistent and stable supply of raw materials and sustained demand from packaging and moulding plants. Recycled content is a legal requirement and assures a market for quality recycled granules.

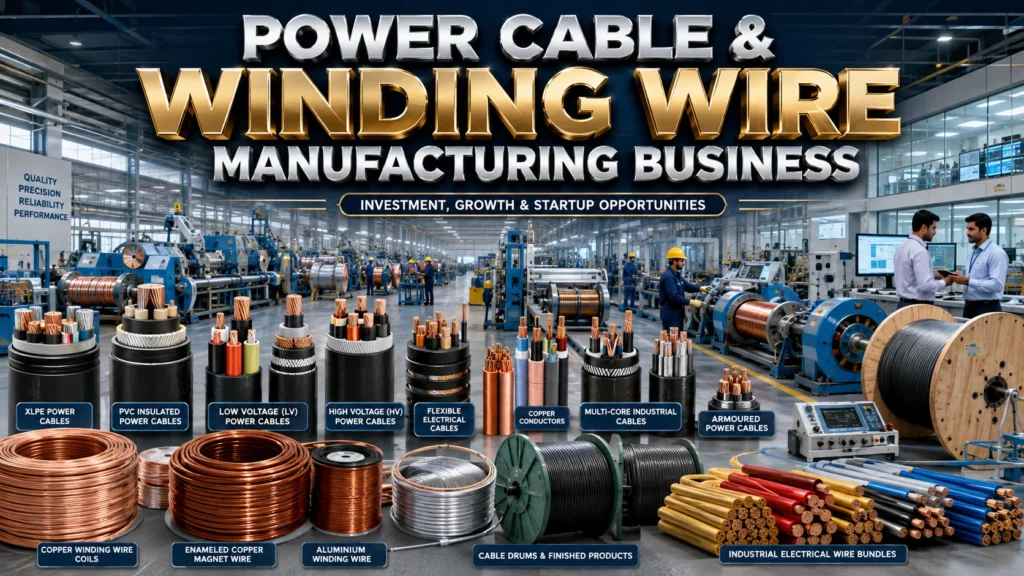

How to Start Power Cable and Winding Wire Manufacturing Business: High-Demand Business Ideas in India’s Electrical Conductors Sector

Power Cable Manufacturing Business Business ideas do come in cycles. There are also companies that are part of the cycle. Power cable and winding wire factories are in second category. Conductors are used every kilometre of transmission line, every substation commissioned, every transformer wound, every motor assembled and every industrial building electrified. The power cable, control cable, winding wire, and specialty conductor segments of the Indian electrical conductor market together account for tens of thousands of crores per year and have seen compounded growth across a number of fronts. Cables and winding wires combine a large and dynamic market, government initiatives to boost domestic manufacturing, a well-defined opportunity for import substitution at the specialty end, multiple product entry points at varying investment scales, and significant future opportunities for entrepreneurs to assess, making them an attractive manufacturing business idea for an MSME. However, there are some challenges inherent in the sector, particularly the prices of copper and aluminium which are benchmarked and volatile throughout the world; but experienced manufacturers overcome this by using commodity hedging, by timing purchases and by passing through material cost fluctuations to customers. Get Detailed Insights from This Book: Manufacture of Electrical Cables, Wire and Wire Products Handbook Why This Manufacturing Business Is Growing at an Exceptional Pace The power transmission and distribution in India is experiencing the most forward-thinking investment cycle in its history. The National Electricity Plan calls for installing more than 50,000 circuit kilometres of transmission lines within 10 years’ time. Particularly in urban areas, the underground cabling of distribution networks is creating a persistent demand for underground LT and HT cables in all key metropolises under the Revamped Distribution Sector Scheme (RDSS). The amount of conductor needed on cabling for each kilometre of length of underground cable is significantly greater than that of lines of a similar capacity on the top of the tower. There is an alternative demand engine from the renewable energy industry. Solar parks need DC cables from panel strings to the inverter and AC cables from the inverter to the point of connection to the grid. Several thousand kilometres of cable might be used in a 100MW solar installation. The wind farm network needs flexible wind farm cables buried and armoured cables in the turbine towers. The Indian target of 500 GW of renewable capacity equates to a demand for the industry to meet at home, which it is actively working on. Enamelled copper and aluminium wires for transformers, motors and generators are also experiencing a surge in demand. Winding wire is used for every new transformer made. Each EV motor needs a certain type of enamelled copper wire. Winding wire is utilized with all types of industrial motors, home appliances compressors and generators. Winding wire demand is directly linked to the growth of the domestic transformer, motor and EV component manufacturing. The demand for winding wire goes hand-in-hand with the growth of the domestic transformer, motor and EV component manufacturing. This is an actual inflection point in the sector. Export Opportunity: Indian Cable Manufacturers Are Winning Global Orders Indian power cable manufacturers are adept at exports and have established a strong presence in the power cable market in Africa, Middle East, and Southeast Asia. The data obtained from EEPC India reveals that engineering exports, such as cables and conductors, have been growing steadily. The UAE, Bangladesh, Kenya and Tanzania are some of the countries that import large quantities of Indian cables. A well certified MSME manufacturer can generate some good export revenues which when added up can give a good cushion against the price fluctuations of the domestic market, especially with regard to exporting IEC certified cables from India as compared to the Chinese and the European options in many of the export markets. Government Policies and Incentives for Cable and Wire Manufacturers BIS Certification: Mandatory and a Market Advantage All power cables delivered to Indian utilities, government projects and big power plants have to be BIS certified. PVC Insulated power cables are covered by IS 1554. XLPE-insulated cables are covered in IS 7098. IS 8783 is applicable to flexible cables. IS 13730 is the standard for winding wires. Although it involves some upfront cost for type testing and factory evaluation, BIS certification can bring benefits such as preferential bidding in Government tenders and deliver credibility in terms of quality to the private sector buyers. BIS certification provides the domestic cables with a score advantage when public tenders are evaluated in accordance with Make in India approach. MSME Support Schemes The Ministry of MSME’s CGTMSE scheme has been introduced to provide working capital and term loan assistance without any collateral up to Rs 5 crores, which is very crucial for the cable manufacturing industry as copper and aluminium are the major expenditure items and the working capital. Upgrading the existing equipment with modern extrusion and wire-drawing machines is supported by the Technology Upgradation Fund Scheme (TUFS). There are two other state level subsidy schemes for electrical conductor manufacturing units under the name of capital subsidy in Rajasthan, Gujarat, Uttar Pradesh and Telangana. PLI and Domestic Content Policy Ministry of Heavy Industries has been actively encouraging the production of electrical componentry at home with PLI-adjacent support schemes. Remarkably, some of the state electricity boards have adopted local content clauses in cable procurement tender that mandates a percentage of locally made cable, which directly benefits Indian MSMEs manufacturers. Duty drawback benefits are also available for exported cable products by Directorate General of Foreign Trade (DGFT), which makes export-oriented manufacturing models more economical. Business Ideas in Power Cable and Winding Wire Manufacturing Business Idea 1: LT Power Cable Manufacturing (Up to 1.1 kV, PVC and XLPE) The low-tension power cable market segment is the widest and most accessible cable manufacturing market, and includes 1.1 kV power cables with PVC insulation (widely used, lower cost) and 1.1 kV power cables with XLPE insulation (higher capacity, longer service life, preferred by utilities). The uses of LT cables are vast in the field

How to Start Empty Capsule Manufacturing Plant in India: Cost, Investment & Profit

Each tablet that is not produced is a capsule order and each capsule order requires an empty capsule before the first milligram of active ingredient is placed in the capsule. However, India’s low bulk capsule production market is concentrated with just a few large-scale manufacturers, with mid-size formulation companies and nutraceutical brands waiting for days for orders which would fill their weeks in a free competitive market. It is the space where India businessmen can create an empty capsule manufacturing plant that can be sold to other business-to-business players – not branded as a consumer product. It’s packaging-adjacent manufacturing — not sexy, not obvious to the purchaser, and not a business that first-generation entrepreneurs typically think about. The vegetarian and HPMC capsule market is expanding more quickly than the domestic supply, due to the demand of halal, kosher and vegan consumers, which can’t be met by the gelatine capsule market. Get Detailed Project Report (DPR): Empty Gelatin Capsules Why This Is a Genuine Opening In this case, the demand reasons aren’t based on convincing anyone of anything. All tablet manufacturers making the move to capsule dosage, all new supplement brands from the nutraceutical industry, and every export order from Africa or Southeast Asia requires a dependable capsule supplier, but the supply base at home has not been able to keep up with the increase in formulation and nutraceutical manufacturing it feeds. There’s a special challenge for vegetarian HPMC capsules: consumers’ growing preference for plant-based shells for religious, dietary, and ethical reasons has created a shortage that’s exacerbated by the fact that only a few Indian manufacturers are currently producing HPMC capsules on a scale that meets demand. The entry cap-ex is not negligible. The cost of the single-line hard gelatin capsule unit, which is capable of producing about one billion to 1.5 billion capsules a year, is about eight to 15 crore rupees, involving investment in dip-pin machines, drying tunnels and printing equipment. The processing and drying conditions for the polymer used to make capsule lines are significantly different from those used in the case of gels and the lines are therefore more expensive, fifteen to twenty-five crore rupees. FSSAI registration is required for licensing and in case of export oriented pharmaceutical formulators, facility approval from CDSCO or USFDA clearance is required, which takes around twelve months of the commissioning process. Margin and Risk Structure This is because the commodity hard gelatin capsules is a thin margin business itself (gross margins are 8-12 percent) and because buyers change suppliers by fractions of a rupee per thousand capsules. The gross margin on HPMC vegetarian and specialty capsules is very high, anywhere from 18-25% gross margin, due to the fact that far fewer manufacturers can reliably produce these capsules to pharmacopeia specification, allowing the early movers to really have the pricing power that commodity gelatin manufacturers do not. In this segment, scalability typically comes from installing lines, not from building new facilities — a founder typically launches with a handful of dip-pin machines, tests out quality uniformity with a few formulation buyers, then expands lines based on repeat demand. The primary risks are raw material dependent; the price for gelatin is tied to the prices of bone and hide collagen on the global market, and is liable to sudden fluctuations, while HPMC is a derivative of cellulose, with a smaller and more concentrated global base of suppliers for its raw polymer. The other risk is rejection by quality-sensitive pharmaceutical buyers; if a buyer orders a year’s worth of sales but finds that one batch is out-of-specification, he or she may not order the next one. Product and Project Opportunities Worth Evaluating Standard Hard Gelatin Capsules The standard hard gelatin capsules are by far the biggest share of the market, providing generic pharmaceutical formulations to the overcrowded manufacturing camps in Baddi, Hyderabad and Ankleshwar in India. A unit designed to serve 1-1.5 billion capsules per year requires capex of ten to fourteen crore rupees, with an expectation of supplying companies in the formulation business within a radius of 300-400 kilometres to ensure cost of logistics. With the strong competition in the price of the existing large suppliers, it is obviously not a margin play that the new entrants can make the economics work with, but a business model based on volume and reliability. Gross margins finally settle at 8-12 percent. Related Article: Building a Successful Pharmaceutical Manufacturing Business HPMC Vegetarian Capsules For nutraceutical brands, halal and kosher export buyers, and pharmaceutical formulators seeking alternatives to animal-derived capsules, HPMC vegetarian capsules are the right choice. A dedicated line, which costs between a hundred and two crore rupees, accounting for the specialised polymer-processing and humidity-control specifications, directly targets nutraceutical contract manufacturers and export-based supplement brands. Margins are 18-24 % which is significantly better than gelatin, since there is very limited number of qualified HPMC capsule manufacturer in India till now with a growing demand. Colored and Printed Specialty Capsules Colored and custom printed capsules meet the brand differentiation needs of nutraceutical and consumer wellness companies looking to achieve a white shell that stands out on the shelf. Print and multi-colour capability is an additional cost of 2-4 crore rupees over the existing capsule line, margins are between 20-28 percent as the pricing is done based on brand value and not on the economics of capsules. A good second phase addition for an existing base gelatin or HPMC brand with a founder who does not want to invest in an additional facility for the higher margin brand-conscious consumers. Enteric-Coated Capsule Shells The enteric coated shells, which resist stomach acid and only open up in the intestine, appeal to a more niche but higher-value pharmaceutical and probiotic buyer segment. The additional cost of a specialised coating line at an existing capsule plant is of the order of Rs.5 to 8 crore, and margins are 25-30 per cent due to the technical barrier to entry, where the ability to replicate the coating consistency is a skill that

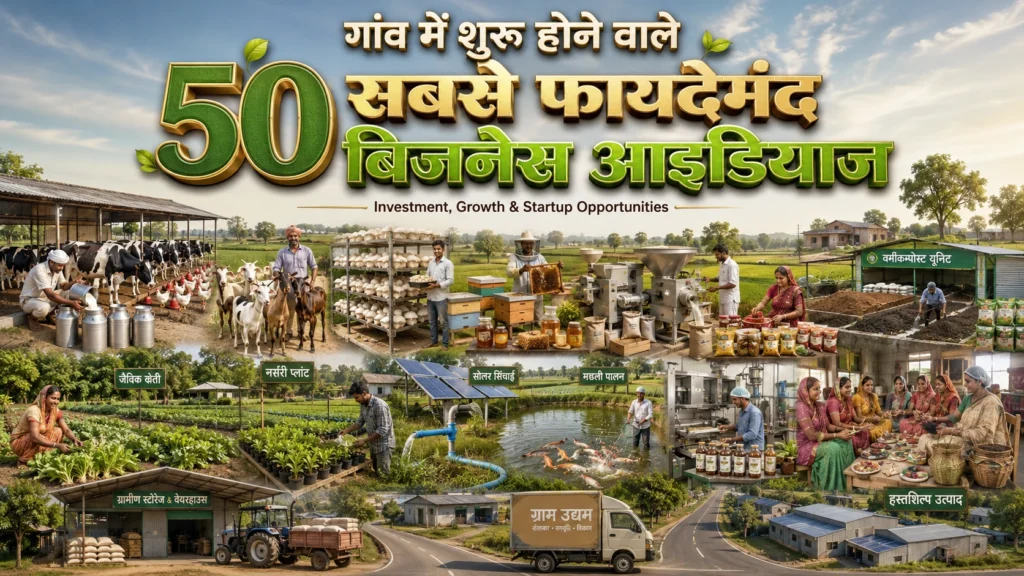

गांव में शुरू होने वाले 50 सबसे फायदेमंद बिजनेस आइडियाज़

गांव में बिजनेस आइडिया भारत के गांवों में एक बड़ा आर्थिक बदलाव चल रहा है। जमीन सस्ती है। मजदूरी कम है। कच्चा माल करीब है। और सरकारी योजनाएं पहले से कभी इतनी अनुकूल नहीं थीं। एमएसएमई मंत्रालय के आंकड़ों के अनुसार देश के कुल सूक्ष्म, लघु और मध्यम उद्यमों का करीब 51 प्रतिशत ग्रामीण और अर्ध-शहरी क्षेत्रों में काम करता है। नाबार्ड की वित्तीय समावेशन रिपोर्ट बताती है कि ग्रामीण परिवारों की औसत मासिक आय पिछले एक दशक में दोगुनी से ज्यादा हो चुकी है। यह रिपोर्ट उन 50 बिजनेस की बात करती है जो असल में चलते हैं — और जिनकी व्यवहार्यता जमीनी स्तर पर साबित हो चुकी है। यह क्षेत्र मजबूत स्टार्टअप अवसर क्यों है बाजार की मांग और विकास ग्रामीण खपत लगातार बढ़ रही है। खाद्य प्रसंस्करण, कृषि सामग्री, हस्तशिल्प और हल्के विनिर्माण — सभी में मांग बढ़ी है। हर बड़ी सरकारी योजना एक नई स्थानीय आपूर्ति श्रृंखला बनाती है। सरकारी सहयोग और नीतियां पीएमईजीपी योजना के तहत ग्रामीण उद्यमियों को 25 लाख रुपये तक की विनिर्माण इकाई के लिए 35 प्रतिशत पूंजी अनुदान मिलता है। अनुसूचित जाति, जनजाति और महिला उद्यमियों को यह और अधिक मिलता है। पीएमएफएमई योजना खाद्य प्रसंस्करण इकाइयों को दस लाख रुपये तक का ऋण सहायता अनुदान देती है। नाबार्ड ग्रामीण उद्योगों को कार्यशील पूंजी ऋण और तकनीकी सहायता देता है। जोखिम जागरूकता ग्रामीण बिजनेस में तीन मुख्य जोखिम हैं — कच्चे माल की मौसमी उपलब्धता, परिवहन की सीमाएं और कुशल कार्यबल की कमी। बिजनेस चुनते समय पहले स्थानीय कच्चे माल और खरीदार की पुष्टि करें — फिर पूंजी लगाएं। बिजनेस चयन का तर्क गांव में बिजनेस चुनते समय ‘क्या चल सकता है’ नहीं, ‘यहां क्या टिकेगा’ यह पूछें। मुनाफे की संरचना तीन स्तरों पर काम करती है: पहला — कृषि आधारित प्रसंस्करण: सकल मुनाफा 18 से 30 प्रतिशत, पूंजी कम, बाजार करीब। दूसरा — हस्तशिल्प और वस्त्र: सकल मुनाफा 35 से 55 प्रतिशत, बाजार जोड़ जरूरी। तीसरा — हल्का विनिर्माण (साबुन, मोमबत्ती, कागज थैली): मुनाफा 35 से 60 प्रतिशत, विस्तार संभव। विस्तार का रोडमैप सरल रखें। छोटी इकाई से शुरू करें, स्थानीय मांग सिद्ध करें, फिर बढ़ें। Find the most profitable startup for your investment range 50 फायदेमंद गांव के बिजनेस — विस्तृत विवरण 1. आटा चक्की गांव में हर घर रोज आटा पिसवाता है — यह मांग कभी नहीं रुकती। पांच से दस घोड़े-शक्ति की मोटर वाली छोटी चक्की में डेढ़ से तीन लाख रुपये की शुरुआती लागत है। रोजाना 200 से 500 किलो पिसाई पर सकल मुनाफा 15 से 22 प्रतिशत बनता है। पीएमईजीपी में 35 प्रतिशत पूंजी अनुदान मिलता है। विपणन की जरूरत लगभग शून्य है — ग्राहक खुद आते हैं। 2. दाल मिल अरहर, मूंग, उड़द — ये सभी दालें ग्रामीण इलाकों में बड़े पैमाने पर उगाई जाती हैं। छोटी दाल मिल में तीन से सात लाख रुपये की लागत है। प्रसंस्कृत दाल कच्चे अनाज से 30 से 40 प्रतिशत महंगी बिकती है। मध्यप्रदेश और महाराष्ट्र में ऐसी इकाइयां सालाना पांच से दस लाख रुपये कमाती हैं। उद्यम पंजीकरण के बाद नाबार्ड से कार्यशील पूंजी ऋण आसानी से मिलता है। 3. अगरबत्ती निर्माण घर से शुरू होने वाला जाना-पहचाना सूक्ष्म उद्योग। मशीन और कच्चे माल पर 50 हजार से डेढ़ लाख रुपये। महिला उद्यमियों में यह सबसे लोकप्रिय विनिर्माण बिजनेस है। तमिलनाडु और कर्नाटक में घरेलू इकाइयां सालाना तीन से पांच लाख रुपये कमाती हैं। खादी एवं ग्रामोद्योग आयोग प्रशिक्षण और बाजार सहयोग देता है। सकल मुनाफा 30 से 45 प्रतिशत। 4. मोमबत्ती निर्माण पैराफिन मोम, धागा और सांचों से शुरुआत होती है। 30 हजार से 70 हजार रुपये में इकाई लग जाती है। सजावटी मोमबत्तियां ऑनलाइन बाजार में 150 से 800 रुपये प्रति नग बिकती हैं। त्योहारी मौसम में मांग तीन गुना हो जाती है। देशभर के ऑनलाइन बाजार तक पहुंच सरल है। सकल मुनाफा 40 से 55 प्रतिशत। 5. साबुन निर्माण हर्बल और हाथ से बने साबुन की मांग शहरी बाजार में बढ़ रही है। 40 हजार से 80 हजार रुपये में घरेलू उत्पादन शुरू होता है। नीम, हल्दी, चारकोल — ये सामग्री गांव में आसानी से मिलती हैं। ठंडी विधि से बने साबुन में सकल मुनाफा 35 से 50 प्रतिशत है। सूक्ष्म खाद्य उद्यम योजना में पैकेजिंग के लिए अलग अनुदान उपलब्ध है। 6. वर्मी खाद उत्पादन जैविक खेती की मांग साल-दर-साल बढ़ रही है। 100 वर्ग फुट इकाई से शुरुआत — लागत 15 हजार से 30 हजार रुपये। तीन महीने में पहली खेप तैयार। आठ से 12 रुपये प्रति किलो के भाव पर महीने में 500 किलो बेचना संभव है। कच्चा माल लगभग मुफ्त मिलता है। सकल मुनाफा 40 से 55 प्रतिशत। 7. मुर्गी पालन एवं चारा प्रसंस्करण 500 ब्रॉयलर मुर्गियों से शुरुआत — लागत डेढ़ से ढाई लाख रुपये। प्रति खेप 45 दिन में शुद्ध आमदनी 20 हजार से 35 हजार रुपये। साल में छह खेप संभव हैं। नाबार्ड के कुक्कुट उद्यम पूंजी कोष से वित्त उपलब्ध है। चारा प्रसंस्करण जोड़ने पर मुनाफा और बढ़ता है। Read the Complete Book Here: Preservation of Meat and Poultry Products 8. मधुमक्खी पालन एवं शहद प्रसंस्करण दस बक्सों से शुरुआत पर 25 हजार से 40 हजार रुपये की लागत। प्रति वर्ष 200 से 300 किलो शहद उत्पादन। जैविक शहद 300 से 500 रुपये प्रति किलो बिकता है। प्रसंस्करण और पैकेजिंग जोड़ने पर 600 से 900 रुपये प्रति किलो तक मिलता है। कौशल विकास मिशन और खादी आयोग दोनों प्रशिक्षण देते हैं। 9. पशु चारा निर्माण डेयरी पशुपालन की वृद्धि के साथ गुणवत्तापूर्ण चारे की कमी है। छोटी चारा मिल में दो से पांच लाख रुपये की लागत है। कृषि उपउत्पादों को मूल्यवर्धित चारे में बदला जाता है। स्थानीय डेयरी सहकारी से सीधा आपूर्ति अनुबंध मिलता है। सकल मुनाफा 20 से 30 प्रतिशत। मध्यम आकार की इकाई सालाना 15 से 25 लाख रुपये का राजस्व बनाती है। 10. गुड़ निर्माण गन्ना उत्पादक गांवों में यह सबसे स्पष्ट अवसर है। पारंपरिक क्रशर और उबालने की इकाई में एक से तीन लाख रुपये लगते हैं। जैविक गुड़ शहरी बाजार में 80 से 150 रुपये प्रति किलो बिकता है जबकि उत्पादन लागत 25 से 35 रुपये है। सूक्ष्म खाद्य उद्यम योजना में पैकेजिंग के लिए अनुदान मिलता है।

Top 8 Products from Waste PET Bottles: Business Ideas & Manufacturing Guide

PET bottle recycling business The PET Recycling Opportunity Transformed by EPR Although most commonly recycled plastic in India, polyethylene terephthalate (PET) – clear plastic made for water, soft drink, cooking oil and food packaging – also poses one of the biggest plastic waste concerns for the country. Annually, India generates about 3.5 million tonnes of plastic waste, most of it-60-70%-being collected through an informal network of rag pickers, Kabadiwala networks and small recyclers, and the other 30-40% ending up in landfills, scattered in dumpsites, and often through incinerators. The implementation of EPR – Extended Producer Responsibility – on all plastic packaging producers in the 2022 Plastic Waste Management Amendment Rules has shifted the economics of PET recycling. Now it comes down to the brand owners to prove they collected and recycled the same amount of plastic they added to the market. This has changed the price of recycled PET from a commodity to an EPR compliance tool, with a lower price limit — thus enhancing the investment argument for formal PET recycling. The current trend of entrepreneurs entering this sector has both genuine demand for the product and value of the raw material driven by the regulations. Related Article: Packaged Drinking Water with PET Bottles The PET Recycling Value Chain PET recycling is a chain starting from collection and sorting by colour (clear, green, blue), followed by baling, washing (hot wash lines remove labels, adhesives and contaminants), flaking (shredding into clean PET flakes) and ending with the conversion of PET flakes into end products. The cost of the investment increases significantly at each step downstream — a “baler” costs Rs. 5 lakhs, a hot-wash line Rs. A fibre spinning line Rs. 50 – 150 lakhs. But so do the margins, 3–8 crore. Entrepreneurs may join anywhere and can sell semi-processed material to the downstream processors or can go forward to get more realisation. Top 8 Products from Waste PET Bottles 1. rPET Polyester Staple Fibre (PSF) The most significant end product from PET bottle recycling worldwide is recycled PET polyester staple fibre. After being washed and dried, PET flakes are melted, extruded through spinnerets, drawn, crimped and cut into short fibers (32-64 mm) that are used as pillows, quilts, sleeping bags, stuffed toys and automotive seat cushions. As European and US brands make their recycled fibre content commitments, the demand for exported materials continues to rise.As Europe and the US brands make commitments to recycled fibre content, the demand for exported materials continues to rise. The cost of 10 TPD rPSF plant is Rs. The stake he has in 2–5 crore and the money he generates is Rs. 60,000–90,000 per tonne of output. Explore This Book: The Complete Technology Book on Expanded Plastics, Polyurethane, Polyamide and Polyester Fibres 2. rPET Polyester Yarn and Fabric The high-quality PET flakes are melted and extruded to continuous filament polyester yarn. These high-quality yarns have a range of uses that include fabrics for Apparel, such as active wear, outerwear and linings, Home & Lifestyle, Home & Technical products. As, many globally recognised fashion brands set recycled targets for Polyester, to some extent that you’re more likely to find some of the leading companies making commitments, you could even be looking at, like adidas, H&M, Patagonia and IKEA setting some standards. Indian rPET yarn manufacturers who cater to these brands have established their export business. When making a rPET yarn spinning Plant, the following is required: This makes it a cheaper product than the other 3–8 crore which produces yarn at Rs. 80,000–1,20,000 per tonne. 3. Food-Grade rPET Resin (Bottle-to-Bottle) The most profitable PET recycling process is the bottle-to-bottle process, where rPET (recycled PET resin) is used to make food-grade resins for new beverage bottles. To get the required high intrinsic viscosity for bottle resin, this will need Solid State Polymerisation (SSP) equipment. There is a considerable investment (Rs. The price of food-grade rPET resin is Rs. 10–25 crore. The price of 80,000 to 1,10,000 per tonne is almost comparable to virgin PET resin price, and raw material (PET flakes) price is much lower. Domestic food-grade rPET is a preferred option as beverage brands under EPR pressure look to fill supply chain. 4. Geotextiles and Technical Fabrics Needle-punched geotextile fabrics used in road constructions, slope stabilisation and soil erosion control are made of rPET fibres. The rPET geotextiles have similar performance to virgin polyester but with a price reduction of 20-30%, which is appealing to infrastructure contractors. Specifying geotextile use is increasing the demand, especially from NHAI and state highway departments. The cost of rPET needle-punch geotextile line is Rs. The value is in the range of 1.5–3 crore and directly serves infrastructure supply chains. 5. PET Strapping Bands rPET flakes can be used directly in packaging and logistics industry for PET strapping. The use of PET strapping has been largely superseded by the use of steel strapping because it is lighter, it is rust-proof and it does not break on impact. The price of a PET strapping extrusion line is Rs. The cost of 30–80 lakh and produces strapping at Rs. $60,000-$80,000 per tonne — for large domestic packaging and logistics industry. Get Detailed Project Report (DPR): Plastics, Polymers & Resins Manufacturing Projects 6. Polyester Resin for Paints and Coatings By performing glycolysis on PET waste, bis-hydroxyethyl terephthalate (BHET) and mixed glycol terephthalate oligomers can be used as polyol for polyurethane foams, alkyd resins and polyester resins in paints and coatings. This is a chemical recycling step which needs more advanced chemistry (Rs.). High value-added chemical intermediates having better margin profiles than mechanical recyclables can be generated (1–3 crore). 7. 3D Printing Filament (rPETG) These PET flakes can be extruded and spooled into filament for desktop FDM printers, which are usually made in a high clarity varnish. The niche, high value application fetches Rs. 3,000–6,000 per kg of filament versus Rs. A value multiplier of 40–75x 60-80 per kg of input PET flakes. Small-scale production (Rs. The 20–50 lakh price segment is aimed

Top 8 Products from Dairy Whey and Cheese Waste: Business Ideas & Manufacturing Guide

Dairy Whey Processing Business Whey — India’s Most Wasted High-Value Food Industry By-Product India is the world’s largest milk producer, with 220 million tonnes of milk being produced annually. The dairy processing industry generates huge quantities of Paneer, Cheese and Casein in the country and along with each of the above product comes a waste stream which is literally being dumped by most of the processors. The liquid end of cheese, paneer, and casein is called whey, which contains about 6.5 grams of protein (in the form of beta-lactoglobulin, alpha-lactalbumin, immunoglobulins and lactoferrin) that are among the most highly nutritious and most rapidly absorbed proteins in human nutrition. About 13-15 MT of whey is produced in India every year due to paneer, chhena and cheese production. If whey protein concentrate (WPC-80) prices are Rs. The protein content in India’s wasted whey is Rs. 400-600 per kg. 5,000 crore+ annual opportunity. The opportunity for specialised whey processing entrepreneurs who can collect, process and supply to the booming sports nutrition, infant formula and pharmaceutical market in India is created by most of the small and medium dairy processors lacking in capital and technology to recover this value. Get Detailed Insights from This Book: Milk Processing & Dairy Products in India Market Research Report The Whey Processing Chain and Entry Points The technological development of whey processing includes collection from the dairy processors (sweet whey or acid whey), pasteurisation, pre-treatment, ultrafiltration (UF) to concentrate protein, spray drying for whey protein concentrate (WPC-35, WPC-70, WPC-80) or further ion exchange chromatography for whey protein isolate (WPI-90). The protein content as well as market value increases significantly at each step. Lactose from the UF (permeate) will be a separate product stream, as lactose powder for pharmaceutical and food applications. This can be done by entrepreneurs at any stage of their business, whether they are interested in selling the semi-processed concentrate to existing driers or they would like to participate as fully-fledged companies and generate finished products for the consumer-market. Top 8 Products from Dairy Whey 1. Whey Protein Concentrate (WPC-80) WPC-80, which contains 80% protein, is the most popular sports nutrition ingredient on the world market, and the main raw ingredient in protein bars, shakes, meal replacement powders and functional foods. Currently, India sources most of its WPC-80 imports from New Zealand, Australian, Europe and the USA. Reprocessing Indian dairy whey domestically would be extremely cost competitive. The cost of a 5 MTPD WPC-80 plant (ultrafiltration + spray dryer) is around Rs. The revenue that the 5–15 crore earns is Rs. 400–600 per kg. 2. Whey Protein Isolate (WPI-90) The highest quality sports nutrition ingredient, WPI-90 is protein-rich, with 90% protein or higher and is faster digested than WPC, low in lactose, and virtually fat-free. An extra ion exchange chromatography/microfiltration step is needed for production in addition to the step required for WPC production. WPI sells at Rs. India’s sports nutrition market (estimated Rs. The value of the market (12,000crore by 2026) is expanding by 15-20 per cent per year, and it is highly import-dependent thereby offering significant opportunity for domestic manufacturing. Build a profitable business with the right idea 3. Whey Powder (Food Industry Grade) Sweet whey powder (12% protein, 70% lactose) is obtained by the simple spray drying of the concentrated whey without protein separation. It is used in bakery products, confectionery, infant formula, animal feed and processed cheese. At Rs. Whey powder is the cheapest product available but is the lowest value product with requirement of Rs. 80-150 per kg. Installing a spray dryer unit for Rs 80-200 lakh, which is an entry point for dairy processors producing whey. 4. Pharmaceutical Lactose Lactose concentration in the permeate from whey ultrafiltration is 4-5%. Crystallised and dried lactose is used in the manufacturing of pharmaceutical tablets as an excipient, in infant formula as well as confectionery and as a fermentation substrate. Lactose is sold at a price of Rs. per unit in Pharmaceutical Grade. The import prices of 150-250 per kg are high and India is importing a huge amount. The cost of a lactose crystallisation and drying unit is Rs. The market is large and import-substitutable, and they are at 2-5 crore. 5. Lactulose (Pharmaceutical Laxative) Lactulose is formed by alkaline isomerization of whey lactose. A pharmaceutical grade laxative and prebiotic for treating hepatic encephalopathy, selling more than USD 500 million world-wide each year. Currently, India depends on the imports of lactulose from Europe. A lactulose synthesis unit (Rs.) The market potential of 3-6 crore for converting lactose from whey into the pharmaceutical product is a very high margin specialty chemical opportunity with good import substitution potential. 6. Whey-Based Animal and Aquafeed Liquid whey can be spray dryed into whey-enriched animal feed pellets without protein concentration for poultry, swine and aquaculture. A fishmeal replacement ingredient which has been shown to improve fish growth. Due to the trend towards dairy and plant protein-based fishmeal alternatives, whey-based aquafeed is becoming an increasing share of the market. Investment: Rs. For blending and pelletising Rs 20-60 lakh. 7. Lactic Acid from Whey Permeate Whey permeates, containing abundant lactose, can be subsequently fermented by Lactobacillus species to yield lactic acid, which can be used in bioplastic (PLA) production, food acidulants, personal care products and pharmaceuticals. The price of lactic acid is Rs. 80–150 per kg. The price of a 100L whey fermentation and lactic acid recovery unit is Rs. 1-3 crore and is linking dairy waste processing to the rapidly expanding bioplastics value chain. 8. Biogas from Whey and Dairy Effluent Whey and wash water from dairy are good substrates for biogas digestion as they have very high BOD value (35,000-60,000mg/l). The effluent from dairy processing plants must be processed legally before discharge. The biogas digester helps in reducing electricity bill and energy cost in ETP compliance by using whey and dairy effluent as raw material to generate biogas as a fuel to provide energy for boilers. Dairy wastes produce biogas, which is also eligible for benefits under

Indian Aluminum Ingots: Market Size, Demand, Market Gap, Major Players, Import-Export Trends & SWOT Analysis, Startup Opportunities and Forecast 2026–2033

Aluminium Ingots Manufacturing Business MARKET INSIGHT With a market size of USD 15.49 billion, India’s aluminum market is set to be valued at USD 25 billion by 2030 growing at a CAGR of ~7.8%. The primary production capacity stands at 4.1-4.2 million tonnes per annum and the domestic demand remains around 4.5 million tonnes per annum thus giving indications of growing demand outstripping the production growth, primarily driven by the downstream ingot consuming sectors. Executive Overview: Why Aluminum Ingots Demand a Closer Look Aluminum ingots are at the heart of India’s most promising industrial aspirations. Where they go, they are the feedstock that enters automotive die-casting workshops, power cable factories, curtain-wall factories in the construction industry, packaging factories, and now, with growing urgency, they enter the electric vehicle supply chain. Each and every structural aluminium window frame, each and every EV battery housing, each and every ACSR power conductor, and each and every beverage can starts its manufacturing life as a cast ingot. It’s not just an academic pursuit—it’s a business imperative for anyone looking to embark on a manufacturing journey in India’s booming metal landscape. India finds itself in a very peculiar scenario in the aluminium value chain. It is the second largest primary aluminium producer in the world with production contributing nearly 6% of the world production. However, India is also one of the major importers of aluminium products. This dichotomy of high production capability coupled with increased import reliance in certain downstream areas, is an indication of structural gap that can be filled up by an entrepreneurial investor with a well-planned manufacturing unit. Data recorded by Aluminium Association of India shows that the nation has about 3.29 billion tonnes of bauxite reserves, making it one of the world’s largest bauxite reserves. Based on this resource base, the future supply of raw material for domestic aluminum ingot manufacturers is more secure than in most competitors’ economies. Market Size, Growth Trajectory, and Forecast 2026–2033 The India aluminium market was valued at USD 15.49 billion in volume terms of around 6,626 thousand metric tonnes. Independent market forecasts determine that the market will clearly grow to USD 25.03 billion by 2030 at a CAGR of 7.81%, while the volume will exceed 10,200 thousand metric tonnes by 2030. The cumulative growth pattern is also quite attractive over the long forecast period to 2033. All forms of aluminium product—rolled sheet, extrusions, foils and ingots are included. But the base product from which all other aluminum products are derived is aluminum ingots. The global aluminum ingots market size is estimated to be more than USD 154 billion in 2023 and is expected to reach USD 205 billion by 2033 with a CAGR of 3.1%. The Indian share is growing very fast in this global market, fuelled by the combined forces of growth of domestic demand and participation in export markets for the downstream products. The global aluminum ingots market was segmented on the basis of the source of their production into primary ingots and secondary ingots, with primary ingots constituting about 62% share of the market by volume. Secondary ingots – made from recycled aluminium scrap – are expanding even more rapidly at 5.32% CAGR, as the world moves towards the principles of a circular economy and the economics of recycling, which uses 95-98% less energy when compared to primary smelting. Get Detailed Project Report (DPR): Complete Aluminium Manufacturing Guide Key Market Indicators: India Aluminum Ingots Sector Indicator Data Point India Aluminum Market Value (Current) USD 15.49 Billion Projected Market Value (2030) USD 25.03 Billion Market CAGR (2025–2030) ~7.81% Primary Aluminum Production (Annual) 4.1–4.2 Million Tonnes Domestic Consumption ~4.5 Million Tonnes per annum India’s Global Production Share Approx. 6% of World Output Aluminium Ingot Imports (Alloyed, 2024) ~240,000 Tonnes (45% surge YoY) Secondary Aluminum Market CAGR 5.32% (Global); 8.5% India Cast Alloys India’s Aluminum Export Value USD 7.25 Billion (COMTRADE) India’s Aluminum Import Value USD 7.67 Billion (COMTRADE) Demand–Supply Gap: The Core Business Opportunity DEMAND–SUPPLY GAP HIGHLIGHT In India, consumption of primary aluminium was 4.5 million tonnes while production was 4.15 million tonnes. The import of alloyed ingots grew by 45% in one year to 240,000 tonnes. This domestic demand of the unmet part is especially for secondary alloy ingots used in the die casting of automobiles, which are the most obvious sign of investment in the Indian non-ferrous metals market. The demand-supply imbalance in Indian aluminium ingots does not exist in isolation, but rather at two different levels. India has 4.15 million tonnes of production of primary ingots, which is more than the country directly absorbs; a large number of primary ingots and unwrought aluminium are exported. But at the secondary and alloy ingot level, the local supply is so low that it is inadequate. According to Big Mint data, and as reported by Al Circle, in just one month, India imported 38,700 tonnes of aluminium ingots, which is 70% higher than the previous year’s figure. The surge on the imports is almost entirely due to the automotive die-casting business, with particular emphasis on the ADC12 and A356 alloy ingots, which are used for EV battery enclosures, suspension components, engine blocks and transmission housings. Some 1.2 million tonnes of aluminum were used in India for automotive applications in a year, and this demand has been rising drastically because of increased electrification of vehicles. EVs consume as much as 250 kg of aluminum per unit, whereas conventional internal combustion engine vehicles only require 150 kg of aluminum per unit. The demand curve of secondary aluminium alloy ingots is practically vertical in India, where the adoption of electric vehicles is expected to hit 30% mark by 2030. This leaves a textbook disparity between supply and demand for entrepreneurs to deal with: there is a big demand for Indian-made alloy ingots of consistent specification from domestic OEMs die-casters and component manufacturers, but there is not a corresponding growth in secondary smelter capacity in India. The outcome is importing dependence: a signal for the market which

India Cargo Shipping Containers Market 2026–2033: SWOT Analysis, Demand-Supply Gap, Startup Opportunities & Government Incentives

India Cargo Shipping Containers Market The India cargo shipping containers market is estimated to be valued at USD 20.5 billion and is projected to reach USD 31 billion by 2033 at a CAGR of 4.7%. The current annual handling capacity of India’s major ports is more than 14 million TEUs which is growing at 8–10% annually. Even with this demand scale, Indian exporters have critically low dependence on external sources if the amount of over 95% dry shipping containers used by Indian exporters has to be considered. If the amount of dry shipping containers used by Indian exporters is taken into consideration, then Indian exporters are critically dependent on external sources with an over 95% dependence rate. Domestic container production in India is close to zero and annually, there is a throughput demand of 14 million TEUs. Almost all dry freight containers are imported from China. Indian exporters faced freight rates up to 3-5 times higher, and even waited for weeks for containers in recent times of freight disruptions around the world. This structural deficiency has been reflected in Budget 2026 via the ₹10,000 crore Container Manufacturing Assistance Scheme (CMAS) – a meagre amount of domestic manufacturing capacity compared to actual demand – in 1 million TEU per year over 10 years. Why Shipping Containers Are the Backbone of India’s Trade Ambitions Talking about India becoming a global manufacturing hub is always accompanied by the words like port, freight corridors and logistics efficiency in New Delhi where the policymakers talk about becoming a manufacturing powerhouse. However, there is one infrastructure that does not get the attention it deserves despite its critical role in India’s trade with the world: The simple steel shipping container. Almost 90 percent of the world’s trade in merchandise goods is conducted by sea, and containers are the standard units of steel that enable this transportation. Availability, cost and origin of shipping containers are not logistics foot-notes in a country like India, where the ports process over 95% of the international trade by volume according to the Ministry of Ports, Shipping and Waterways (MoPSW). It is a national priority issue. This is the paradox of the India cargo shipping containers market: very high demand in a one of the fastest growing trading economies, with virtually all shipping containers coming from China. The market opportunity being analyzed is a paradox: high throughput and no domestic production. Get Detailed Project Report (DPR): Business Ideas for Steel Shipping Container Manufacturing India Cargo Shipping Containers Market: Size, Growth & Forecast 2026–2033 India cargo containers market is estimated to hit USD 20.5 billion by 2021 and is expected to grow at CAGR of 4.7% till 2033. If one focuses only on the shipping container manufacturing and leasing business alone, the market is estimated to be in the range of USD 389 – 403 million and will increase to approximately USD 546 – 563 million during the same period. These numbers, however, only tell part of the story. The far more significant measure is ‘containerized throughput’ – an estimated 14 million TEUs (Twenty-foot Equivalent Units) are handled through Indian ports each year, an increase of 8–10% year-on-year. The highest share is accounted for by JNPT, Mumbai near port and the port at Chennai, Mundra and Kolkata. The growth of deep-water terminals, particularly the Vizhinjam International Seaport in Kerala, reflects India’s plans for much greater volume of containers being processed in the coming decade. The India Brand Equity Foundation (IBEF) (www.ibef.org) has been emphasizing over and over that India’s port and logistics infrastructure is undergoing the most transformational shift since liberalisation, and that the port-led development policy is being given a top priority in the midst of this shift – the Sagarmala Programme. Market Segmentation at a Glance Segment Category Key Observation Market Share By Size 40 Feet Containers Dominant for bulk/industrial goods 57.7% By Size 20 Feet Containers Preferred by SMEs for frequent shipments ~35% By Application Consumer Goods Largest revenue share; urbanization-led Dominant By Application Food & Beverages Fastest growing; reefer container demand Fastest CAGR By Application Industrial Goods / Pharma / Healthcare Growing with export clusters Significant By Region Western India (Mumbai/JNPT/Mundra) Highest container throughput nationally Largest SWOT Analysis: India Cargo Shipping Containers Market Any entrepreneur or investor considering entering this industry will need a good SWOT analysis. The advantages are structural in nature and continuously gaining ground, the disadvantages are largely fixable with capital and policy intervention, the opportunities are among the most alluring found in Indian manufacturing and the threats are real but can be managed through strategic positioning. Strengths As one of the top-ten trading countries in the world, India has an in-built and continuous demand base for containers. The Sagarmala Programme is the country’s port infrastructure modernization initiative which is being implemented at a scale of lakhs of crores. Now, transit time has considerably been reduced through Dedicated Freight Corridors (DFCs) — Eastern and Western corridors — and intermodal container movement is much more economical. Moreover, India boasts a significant steel manufacturing ecosystem with steel producers such as SAIL, Tata Steel and JSW Steel that can provide raw materials at internationally competitive prices for the production of containers. Weaknesses The biggest drawback is the lack of domestic capacity to produce domestic containers. The number of containers that India makes is an insignificant percentage of the containers that it consumes, and more than 96% of the world’s container production is controlled by China. It is a vulnerability of the supply chain that became painfully apparent during the COVID-19 pandemic and subsequent global freight disruption, when Indian exporters paid a freight rate three to five times greater than normal rates and were forced to wait for weeks for shipments because containers were scarce. The industry also does not have a skilled fabrication labor force to assemble high volume of steel containers for marine applications. Opportunities Changing opportunities. In the Union Budget 2026–27, the Government announced a ₹10,000 crore Container Manufacturing Assistance Scheme (CMAS) for five years with a

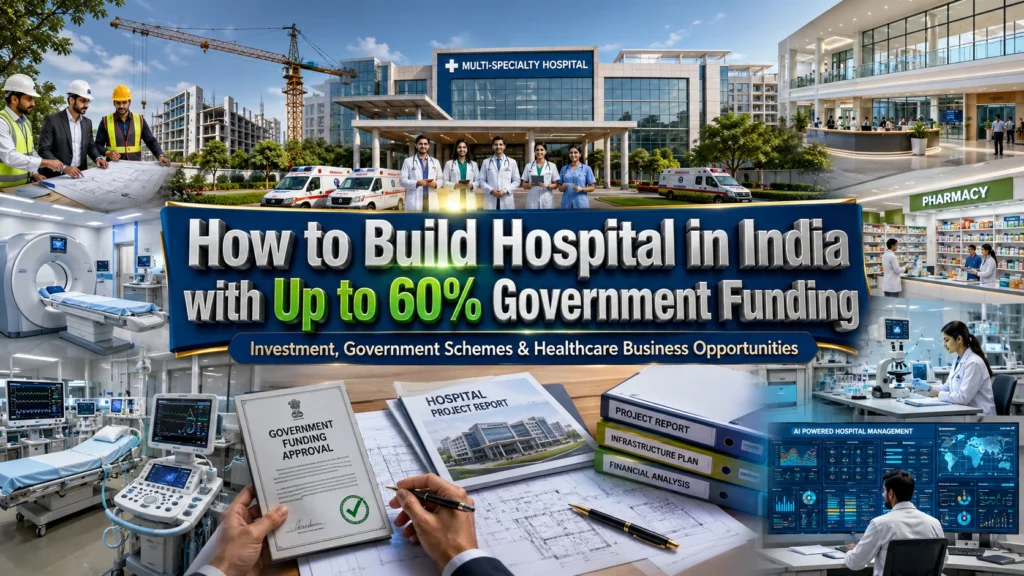

How to Build Hospital in India with Up to 60% Government Funding

Hospital business in India India has a shortfall of more than 6 lakh hospital beds to meet the WHO recommended norms, and the government has put a number of financial instruments in place to address this shortfall — many of which the majority of entrepreneurs are unaware of. When the project is structured properly, the government can provide Rs.25–30 Crore to the hospital through the scheme of Viability Gap Fund (VGF) under the State Government, National Health Mission (NHM) capital funding, Ayushman Bharat Health Infrastructure Mission (AB-HIM) grants, and NABARD concessional long-term loan. These are ideas for businesses in healthcare that are both commercial and directly hit a public national health problem that’s being actively pursued by the government with allocated resources. Why India Urgently Needs Private Hospital Investment India has an average of 0.55 hospital beds per 1,000 individuals, which is significantly below the WHO recommendation of 3 beds/1,000 people. The gap is particularly acute in Tier-2 and Tier-3 cities where the capacity of the public health system is not being utilized optimally. More than 60% of healthcare expenditure is already on the private side in India, clearly showing that patients opt for private care when it’s available and affordable. The Ayushman Bharat PMJAY scheme has opened up insurance coverage for more than 55 crore beneficiaries, leading to assured inflows of patients into empanelled private hospitals provided the hospitals are available in the right places. Health entrepreneurs can use the district level health infrastructure gap data published by the Ministry of Health and Family Welfare to help them choose project locations. Get Detailed Insights from This Book: Investment Opportunities In Hospitality, Medical, Entertainment, Ware Housing & Real Estate Projects Government Schemes That Can Fund Up to 60% of Your Hospital A number of complementary Government schemes are available to be rolled up to finance a substantial part of a private hospital project. The National Health Mission (NHM) PPP component is in charge of funding the initiatives of private hospitals in low-density regions. Different states like Uttar Pradesh, Bihar, Rajasthan, Jharkhand and Odisha provide private hospitals with Viability Gap Funding (VGF), which is a grant of between 20-35% of the project cost that is provided for hospitals investing in district towns where healthcare facilities are inadequate. NABARD offers concessional long term loan facilities at lower interest rates in rural and semi urban areas for healthcare. Thousands of crores have been allocated under the Ayushman Bharat Health Infrastructure Mission (PM-ABHIM) for development of Healthcare Infrastructure with a provision for participation of the private sector. Having VGF grants and concessional NABARD loans along with operational revenue from PMJAY gives rise to a project financial model which makes the entrepreneur’s net capital requirement much less. Top Business Ideas Within the Hospital Development Model 100-Bed District Hospital with Surgical and Emergency Focus Most of the health needs of a population of 10 to 30 lakh people in a district is met by a 100-bed district hospital having a general surgery OT, orthopaedic surgery capability, obstetrics and gynaecology, ICU, NICU and 24×7 emergency services. After considering the state VGF, NABARD debt, the entrepreneur’s investment in equity comes to Rs.18-20 Crore. First Quality Milestone, get NABH Accreditation – mandatory for empanelment with PMJAY and CGHS and will ensure institutional revenue. Fill online application form on the National Health Authority website for empanelment under PMJAY. PPP Model Hospital Under NHM or State Government Concession The most capital efficient model is the Public-Private Partnership (PPP) model where a private operator constructs and operates a hospital in a public land, on the condition that the government will provide him a minimum patient volume or a subsidy for the operation of the hospital. The NHM has issued PPP guidelines that outline the mechanisms of engagement between the NHM and State health departments for district level hospital PPP arrangements. The State Governments in Tamil Nadu, Karnataka, Andhra Pradesh and Maharashtra have well established PPP hospital frameworks. In some state models, the government constructs the building and pays for the equipment and the private operator operates it and delivers clinical services — eliminating the need for a significant investment from the entrepreneur. Get Detailed Project Report (DPR): Healthcare Business Ideas in the Medical Sector Speciality Hospital Targeting One High-Volume Surgical Procedure Single specialty hospitals (cardiac, orthopaedics, ophthalmology or oncology) have better clinical outcomes and financial performance than generalist hospitals for the same size. A 50-bed cardiac care hospital in Tier-2 city can achieve the same revenue as 100 bed generalist hospital given the higher complexity of the procedures, which command premium rates of PMJAY packages. Specialisation decreases the diversity of equipment needed, leading to more efficient capital deployment. Talk to SECI equivalent at NABH for their advice on the speciality hospital accreditation pathways that lead to premium insurance rates. Import-Export Opportunities in Hospital Development There is a high level of import activity because of the development of hospitals — medical equipment’s from Siemens, GE, Philips and Fujifilm. CDSCO portal can be used to verify duty concession on medicals which are lifesaving medicines. The medical tourism industry is a foreign exchange generation sector in India which is growing day by day. A modern, NABH certified well equipped district hospital can be developed to attract medical tourists from Bangladesh, Nepal, Myanmar and the Gulf countries for its quality, affordable care. The Ministry of Tourism has a medical tourism policy that offers marketing assistance for the facilities approved. Indian MSME Success Stories in Hospital Development Narayana Health — Making Super-Speciality Care Affordable at Scale Located in Bengaluru, founded by Dr. Devi Prasad Shetty, Narayana Health challenged Indian healthcare by bringing to light the fact that cardiac surgery, when carried out in a high-volume, processes-driven fashion, can be a major cost-effective and yet world-class experience for every patient. Dr. Shetty’s shrewdness, that high volume would bring cost efficiency as well as improvement of quality, resulted in hospitals being constructed in areas where they were most needed. Narayana Health’s patient volume model was defined around the

India’s ₹5 Crore Food Processing Business: Gulf Export Opportunities for Manufacturers

₹5 Crore Food Processing Business in India The food processing industry in India is at a turning point and for those who are thinking of entering into any serious business in manufacturing, the food processing unit with a capital investment of Rs.5 Crore for export to Gulf countries is one of the most commercially viable business ideas possible today. The Gulf Cooperation Council (GCC) countries – Saudi Arabia, UAE, Qatar, Kuwait, Oman and Bahrain – import billions of dollars in packaged and processed food each year. Geographic advantage of India along with huge population of NRIs in these countries leads to a natural demand pipeline. The Ministry of Food Processing Industries has always identified this as a priority for export and the availability of policy support in terms of capital subsidies and export promotion schemes is as easy as ever. Why the Food Processing Sector Is Booming in India India is the second largest producer of fruits and vegetables in the world but a large proportion of them is wasted because of lack of processing facility. The food processing industry is a significant contributor to manufacturing GDP of India and it is an industry which continues to attract investment from both the domestic and foreign sector. The food import needs of the Gulf countries, especially in Saudi Arabia and UAE, have increased substantially due to the huge rate of urbanization and development of the middle class. Indian processed food, including rice flour, spice blends, and ready to cook mixes, as well as frozen snacks, is always in demand in these markets. India’s agricultural exports have been continuously on the rise, with processed food playing a larger role, according to APEDA (Agricultural and Processed Food Products Export Development Authority). It’s an investment that’s also recession-proof — spending on food by consumers doesn’t slow down when the economy slows down, so consumer demand is always stable. Get Detailed Insights from This Book: Handbook on Fruits, Vegetables & Food Processing with Canning & Preservation Government Policies and Incentives for Food Processing Units Entrepreneurs are provided with several targeted schemes by the Ministry of Food Processing Industries (MoFPI). PMKSY offers capital subsidy to food processing units in clusters up to 35%. The innovative product category and organic product category are included in the Production Linked Incentive (PLI) scheme and are given incentives based on incremental sales. Further, the Credit Guarantee Trust Fund scheme of MSME Ministry has made it possible to avail collateral-free loan of Rs.2 Crore. APEDA is active in facilitating exports to the Gulf market in the following ways: Trade Fairs, Buyer-Seller Meetings, Export Certification. Food Safety and Standards Authority of India (FSSAI) has introduced fast-track licensing for export units, which can cut down the compliance timelines for the entrepreneurs. There are also electricity subsidy and provision of land in food parks by the State governments like Maharashtra, Gujarat, and Punjab. To get a detailed list of incentives available, please see the Startup India portal. Top Business Ideas in Food Processing for Gulf Exports Ready-to-Cook Indian Meal Kits and Spice Blends There are more than 8 million Indians living in the Gulf who are actively looking for real Indian flavours. Production of standardised spice mixtures, masala powder, ready to cook curry base, and meal kits can create a huge export brand with a simple investment. From Rs.5 Crore you can operate an automated blending, grinding and vacuum-packaging line, which complies with Gulf food safety certifications like GCC conformity marks and Halal certification. The two key factors in a supermarket’s success in retail shelf placement in the Gulf are consistency and packaging quality. Generally, gross margins for branded spice blends are between 35% and 50%, and hence this is one of the more profitable categories in the food processing industry. For direct buyer connect opportunities, APEDA’s export promotion programmes are for the benefit of entrepreneurs. Rice Flour, Semolina, and Milled Grain Products Domestic ag capacity is very low due to the arid conditions in the Gulf region which makes them very dependent on import of grains and milled products. This can be met by processing of rice and wheat in India which are available at competitive prices. A milling unit handling a capacity of Rs.5 Crore can mill the paddy or wheat to get refined flour, semolina, rice flour, beaten rice, and value-added grain products. Grain-based products are relatively easy to certify for the Halal markets in the Gulf (notably for the fact that this certification does not impose any extra compliance cost). Shelf life of 12 to 18 months can be obtained with good cold chain and moisture-controlled packaging, which meets the retail distribution cycles in the Gulf. Entrepreneurs should visit DGFT (Directorate General of Foreign Trade) for export documents and for IEC code registration. Your investment deserves the right opportunity Frozen Snacks and Traditional Indian Namkeen for the Gulf Retail Market One of the fastest-growing product line in the Gulf supermarkets is frozen food and packaged snacks. Indian namkeen, frozen samosa, frozen paratha and ethnic snack products have each a separate section in the Lulu Hypermarket, Carrefour and Spinneys in the Gulf. There is an investment requirement for the purchase of industrial fryers/ovens, individual quick-freezing equipment and cold storage packaging lines for setting up a frozen food processing unit at Rs.5 Crore. The unit should be HACCP standards and export-controlled temperatures. Many other Indian companies such as Haldirams, MTR Foods have proven this export model at large scale and enough opportunities are there for regional brands to establish niche positions. Import-Export Opportunity Analysis India has been steadily increasing its food and processed food exports to the Gulf region and bilateral agreements have ensured that most of the food categories have relatively low tariff. The APEDA data also reflects that rice, spices, processed vegetables and ready-to-eat products are the key commodities for India’s food export to the GCC. The UAE is also a re-exportation hub; if an Indian exporter sets up distribution in the UAE, then it is relatively easy to