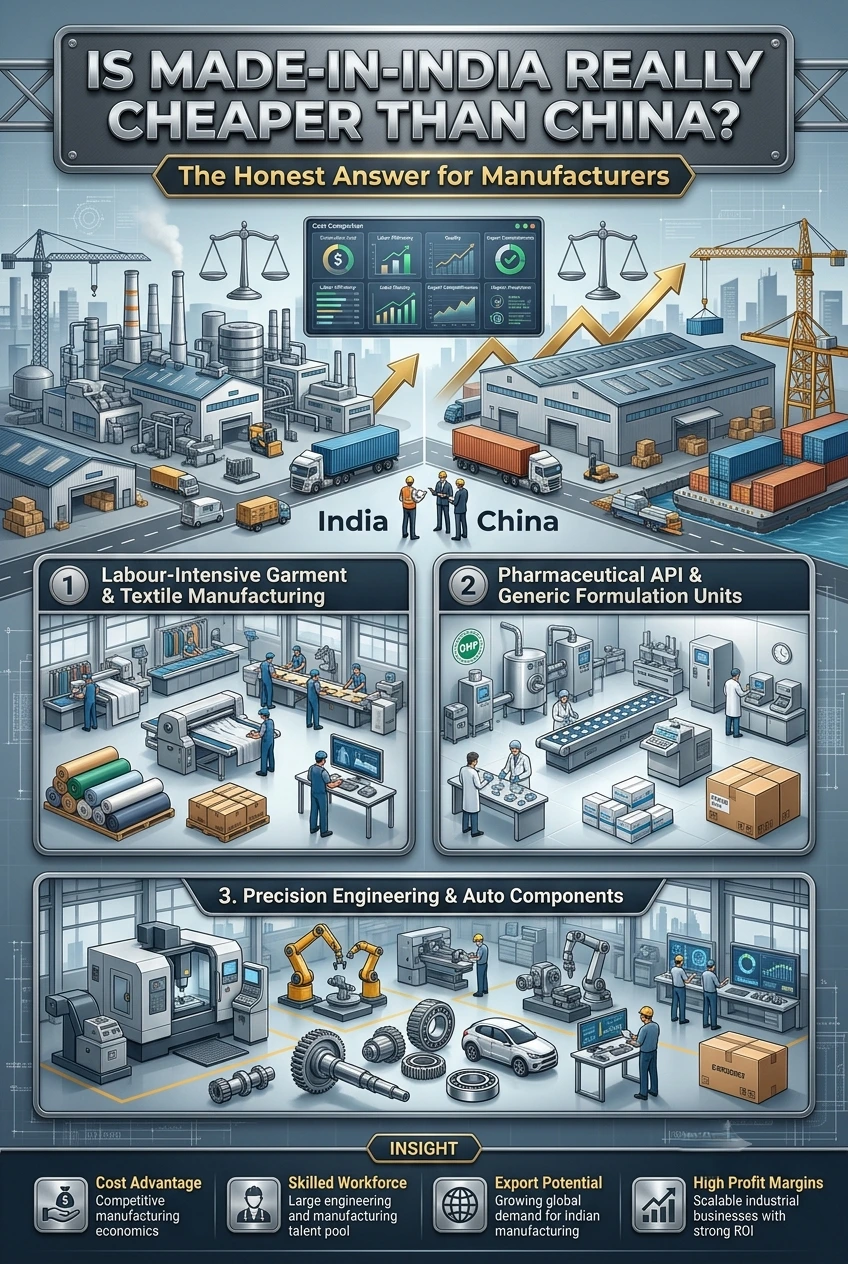

India vs China Manufacturing Cost Comparison

The manufacturing fraternity in India creates a new momentum every few months. Glossy headlines herald factories moving, FDI soaring and a new day of industrial self-reliance. The prospect is alluring: India’s labor cost is less than China’s, government is providing incentives, and the geopolitical winds are favouring us. This is the story that is compelling to start-up founders who are considering manufacturing business ideas, and often is incomplete.

The real answer is more complicated. India may be more cost-effective for a wise choice of product, scale and supply chain setup when compared to China. But for a lot of categories, the hidden inefficiencies, logistics, infrastructure, and lead time for manufacturing in India still heavily compete with China. That’s closing. However, it has not yet closed.

This article cuts through the clutter. It looks at India’s cost advantage, its remaining disadvantage and what considerations manufacturers should make before making a decision on sourcing and/or investment.

Contents

- 1 The Labour Cost Advantage Is Real — But Overstated

- 2 Where India’s Cost Advantage Gets Eroded

- 3 Government Policies and the PLI Push

- 4 Business Ideas Where India Already Beats China

- 5 The Import–Export Opportunity: Where Trade Flows Are Shifting

- 6 Indian MSME Success Stories: What They Got Right

- 7 How NPCS Can Help You Evaluate Manufacturing Feasibility

- 8 India vs China: Manufacturing Cost Comparison by Sector

- 9 Frequently Asked Questions

- 10 Conclusion: The Honest Verdict

The Labour Cost Advantage Is Real — But Overstated

Let’s talk about India’s strengths first. Average manufacturing wages in India are still much lower than the Chinese counterparts. Data collected by the International Labour Organisation (ILO) and trade bodies like CII shows that factory workers in labour-intensive industries in India are earning approximately 30–45% less than their Chinese counterparts in the same job. That’s a lot of benefit on the books, at least.

The industries that benefit most from such an advantage are primarily the clothing, leather, footwear, simple assembly, and some agro-processing industries. For these items, labour represents 35-60% of the total cost. India thus has a defensible cost advantage. It is for this reason that global apparel firms are moving orders to Tiruppur, Surat and Noida. The Confederation of Indian Industry (CII) keeps a close watch on this trend and observes the increasing competitiveness in labour intensive manufacturing.

But there are other inputs than labour. Many new startups begin by focusing on labor expenses for manufacturing and neglecting to factor in other expenses. It is not. In capital-intensive or precision manufacturing, labour may only be 10-20% of the cost.

Related Article: India vs China Manufacturing: Best Business Opportunities, High Profit Sectors & Startup Ideas in India

Where India’s Cost Advantage Gets Eroded

Logistics and Inland Infrastructure

The Pearl River Delta is a marvellous logistics machine in China. Factories are located within 60-100 km of ports with millions of containers moving through them each month. The roads are of excellent quality. Rail freight operates at high speed. All cold chains, warehouses and last mile are scaled.

India’s logistics cost to GDP is in the range of 13-14%, whereas China’s logistics cost to GDP is 8-9% and in developed nations 6-8%. This gap is recognized straight by the Ministry of Commerce and Industry and the National Logistics Policy. The result: manufacturers are paying an additional 4–6% to cover inefficiencies, such as road conditions, port delays and broken cold chains. This one feature can cost the exporter his/her labour cost savings.

Power and Utilities

The power tariffs for industries are significantly different across states in India, but on average are higher than in China. Power cost is the most important variable input in highly energy consuming industries such as steel processing, chemicals, aluminium, ceramics and glass. In these areas, China’s energy subsidy system and integrated utility system provides a structural cost advantage which India is still trying to catch up with.

The Bureau of Energy Efficiency (BEE), under the Ministry of Power, has launched a number of initiatives aimed at enhancing the energy productivity of MSMEs. However, most States still face a tariff deficit against the Chinese industrial zones, and PAT (Perform, Achieve and Trade) cycles and energy audits have helped.

Raw Material Supply Chains

In part, China developed its manufacturing power by clustering together raw material processing, component production, and final assembly. Shenzhen for electronics. Foshan for ceramics. Small goods in Yiwu. India is building similar clusters, such as textile parks, pharma SEZs and electronics PLI hubs, but the level of depth in the ecosystem is still not matching.

India still imports high volumes from China for manufacturers that rely on precision components, speciality chemicals or electronic sub-assemblies. This makes the situation a little paradoxical – a manufactory which seems to be “made in India” can have a partly Chinese supply chain.

Government Policies and the PLI Push

Indian government has acknowledged these deficits. The Production Linked Incentive (PLI) scheme is implemented through DPIIT and line ministries, and has a total allocation of more than ₹1.97 lakh crore in 14 sectors. They range from mobile phones, pharmaceuticals, medical devices, food processing, textiles, white goods to specialty chemicals. The goal is to push the overall disadvantage of the output side towards direct output-based cash payments.

The Ministry of MSME provides credit guarantee scheme (CGTMSE) for MSMEs, capital subsidy on technology upgradation (CLCSS), and the Udyam registration framework which unlocks priority-sector lending for MSMEs. Besides, there’s a Make in India portal (Make in India) which collates information regarding incentives under state and central schemes.

It is perhaps the most effective structural intervention, the PM Gati Shakti National Master plan. It plans and manages road, rail, port and utility infrastructure at an integrated level. If fully operational, Gati Shakti has the potential to bring down India’s logistics cost differential by 3-4 percentage points, thus changing the competitiveness landscape.

Business Ideas Where India Already Beats China

1. Labour-Intensive Garment and Textile Manufacturing

Today, India offers a real cost benefit to entrepreneurs, who are considering their business options in the apparel industry. A well-managed garment unit in Gujarat or Tamil Nadu can compete with the Chinese mills on product categories which are basic and mid-range as the labour cost is 35-40% cheaper compared to the Chinese mills. Additional output incentives are given under PLI scheme for textiles. The success is to establish effective cutting-sewing-finishing lines, to obtain OEKO-TEX or GOTS certification for export markets, and to establish direct buyer-seller relationship without depending on trading intermediaries.

Get Detailed Insights from This Book: The Complete Technology Book on Textile Spinning, Weaving, Finishing and Printing

2. Pharmaceutical API and Generic Formulation Units

One of the most evident instances of import substitution from China is the Indian pharma industry. With its in-depth chemistry expertise, existing cluster infrastructure in Hyderabad and Ahmedabad, and track records of regulation, Indian API manufacturers have become available at competitive prices to the world. The adjoining areas like nutraceuticals, herbal extracts, AYUSH formulations and veterinary APIs are very cost logical for new entrants. The use of raw materials from local botanicals along with the availability of the DSIR-recognised R&D facilities will be cost and IP benefits over Chinese alternatives.

View Full Project Details: Active Pharmaceutical Ingredient (API) Products, Bulk API Manufacturing

3. Precision Engineering and Auto Components

India’s engineering talent is what creates measurable cost competitiveness in the auto component business. Supply ecosystems have been established in clusters in Pune, Chennai, Gurugram and Rajkot. The prices of Indian units can be in line with or less than China, particularly considering the escalating cost of Chinese labor, pricing for quality certification, and ocean freight, for castings, forgings, machined products and sub-assemblies sold to Tier 1 automotive Original Equipment Manufacturers or export markets. New businesses should centre on high-mix, low-volume precision manufacturing where there may be structural disadvantages for China’s standardised factories.

The Import–Export Opportunity: Where Trade Flows Are Shifting

The US-China trade war, diversification of the value chain by European firms, and the China+1 policy of Japanese and Korean multinational companies have provided clear opportunity. In a number of electronics assembly, chemicals and engineering goods markets which traditionally were dominated by China exporters, Indian exporters have captured market share.

As per DGFT (Directorate General of Foreign Trade) data, Indian exports of goods and services combined crossed $770 billion mark in merchandise exports. Increasingly, engineering goods, pharma and chemicals are making up a larger portion of the total. For the startups, it translates to getting into a sector where the global buyers are actively seeking India as an alternate supplier (not backup) and not as a supplier that they are avoiding.

This is also true for the import side. There is a clear opportunity for import substitution in India for Chinese electronic components, speciality chemicals and machine tools. Polynesia and domestic entrepreneurs who develop domestic alternatives in these categories benefit from a captive market, policy tailwinds, pricing leverage, as long as they can meet the quality standards.

Indian MSME Success Stories: What They Got Right

Dixon Technologies — Sunil Vachani

Dixon Technologies started its business as a contract electronics manufacturer, when China ODMs ruled the roost in India’s consumer electronics space. Sunil Vachani’s key takeaway from the entire exercise was the fact that if global and Indian brands had to undertake electronics manufacturing at home to get MRP labelling and then PLI benefits, someone has to develop this capability at scale. Dixon led the way in investing in quality systems, EMS infrastructure, and design capability. It makes mobile phones, LED television sets, washing machines and medical equipment for companies such as Samsung, Motorola and Panasonic today. A lesson for new entrepreneurs is that being placed on the inside of a successful government-backed demand creation scheme, before the market becomes apparent, is a great competitive advantage.

Borosil Renewables — P.K. Kheruka

The Kheruka family group, Borosil Renewables, is a rare Indian manufacturer which has accepted the Chinese solar glass imports. Solar glass is a very capital intensive and competitive product. But Borosil built capacity quickly, made investments in energy efficiency and successfully lobbied for import duty protection on Chinese solar glass. The outcome: a sustainable home-grown supply chain for the Indian solar sector which requires government support. The takeaway: With the right mix of scale investments, policy engagement and customer development, Indian manufacturers can compete in any category.

Suprajit Engineering — K. Ajith Kumar Rai

Suprajit Engineering is one of the biggest automotive cable manufacturers in India with an international presence after acquiring Wescast Industries, based at UK. Suprajit began with domestic auto components supplier in Bengaluru, and after securing volume with Indian OEMs, successfully made a move to export markets. This cost edge over Chinese suppliers in some categories of cables was due to its lean manufacturing, its domestic cable drawing capability and its close proximity to the Indian OEM development cycles. The message: A good Indian MSME playbook is to lay the foundation of domestic business first followed by international expansion.

How NPCS Can Help You Evaluate Manufacturing Feasibility

The most critical issue for entrepreneurs making a cost comparison between India and China is the project level financial analysis and not a general one. At Niir Project Consultancy Services (NPCS), we offer a professional business or industry market survey cum Detailed Techno-Economic Feasibility Reports (DPRs) to establish new industries or business. Detailed manufacturing process, market research and demand analysis, process flow diagram, product mix and capacity planning, machinery and raw material details, complete project financials with profitability analysis are included in our reports.

Our goal is to guide entrepreneurs to assess feasibility, profitability and sustainability within a long-term perspective before they invest. A feasibility report is the first step for sound decision making whether it’s a greenfield plant, an import substitution project, or a PLI connected project.

Discover business ideas that actually make money

India vs China: Manufacturing Cost Comparison by Sector

| Sector | India Labour Cost Advantage | India Logistics Gap | Net Cost Position vs China | PLI Available? |

| Garments & Apparel | 35–45% lower | Moderate impact | India cheaper | Yes |

| Pharma APIs | 20–30% lower | Low impact | India competitive | Yes |

| Electronics Assembly | 25–35% lower | High impact | Near parity | Yes |

| Auto Components | 20–30% lower | Moderate impact | India competitive | Partial |

| Speciality Chemicals | 15–20% lower | Moderate impact | Near parity | Yes |

| Capital Equipment | Minimal advantage | High impact | China cheaper | No |

| Solar Glass / Panels | Minimal advantage | Moderate impact | China cheaper (with duties: parity) | No |

Frequently Asked Questions

Q1. Is India cheaper than China in terms of manufacturing in general?

Not in all sectors. India has a definite edge in labour-intensive industries such as clothing, leather, and simple assembling. In industries that are capital intensive, energy intensive or precision manufacturing, however, the cost difference diminishes or even turns upside down when logistics, power and supply chain depth are taken into account.

Q2. The PLI scheme is a scheme to reduce costs, what is it?

Production Linked Incentive scheme offers direct cash incentives of 4-15% on incremental sales over the base year. It creates effective subsidy for production cost of eligible manufacturers in 14 targeted industries that enhances the competitiveness of India in global markets.

Q3. Which are the sectors that have the highest returns to new manufacturing ventures in India?

Presently, the segment of pharmaceuticals and nutraceuticals, electronics contract manufacturing, auto parts and textile processing are the most promising areas with policy support, domestic demand and export potential. It is advisable for the entrepreneur to conduct a feasibility study before investing money into the business in the selected sector.

Q4. What is the impact of the logistics challenge faced by India on its export competitiveness?

Logistics cost in India is about 13-14% of the GDP while it is 8-9% in China. This equates to increased cost of inland transport, port handling, and lead time expenses for exporters. This is being addressed by the PM Gati Shakti programme and dedicated freight corridors in the coming years.

Q5. What government schemes support MSME manufacturers in India?

The PLI Scheme (by DPIIT), CGTMSE Credit Guarantee (by Ministry of MSME), CLCSS Tech Subsidy, and state MSME industrial park initiatives are a few key schemes. Start-ups need to ensure registration under Udyam and work with the respective state Industry Department to access all combined incentives.

Q6. How do I evaluate whether to manufacture in India or source from China for my product?

The decision requires a product-specific total cost of ownership analysis — covering raw material sourcing, labour, energy, logistics, lead times, minimum order quantities, and working capital cycles. Generic comparisons are rarely actionable. A detailed techno-economic feasibility report provides the structured framework needed for this evaluation.

Conclusion: The Honest Verdict

India is not uniformly cheaper than China. That statement, however disappointing it may sound to enthusiasts, is the honest starting point for good manufacturing strategy.

The advantage India holds is real and growing — in labour costs, in policy support, in geopolitical positioning, and in domestic market depth. However, that advantage is currently concentrated in specific sectors, specific scales, and specific supply chain configurations. For entrepreneurs with the patience and analytical rigour to identify where India’s cost equation genuinely works, the opportunity is substantial.

The manufacturers who will win in India’s next industrial decade are not those who believe the marketing narrative uncritically. They are those who do the hard work of project-level cost analysis, choose the right sector and location, engage government incentive programmes intelligently, and build supply chains that compound India’s natural advantages while systematically closing its gaps.

That is the honest answer for manufacturers. And it is, in the long run, a more optimistic story than the oversimplified version.