Compressed Biogas Export from India

The export India story on compressed biogas is still in its nascent stages but the message is clear. The nation has a huge biomass surplus which can be harvested from agricultural waste, municipal solid waste, dung of cattle etc. which is something that most of the energy importing countries can only dream of. Domestic CBG production is growing and the policy machinery is already geared up for a much bigger play. The CBG-CGD synchronization scheme has led to the successful blending in 54 Geographical Areas of the City Gas Distribution network. The obligation to blend starts in FY 2025-26. Industry is getting regulatory support of this magnitude at an early stage and so is the export potential. India is now not only capable of producing enough CBG but whether entrepreneurs will outpace the other suppliers to catch the global opportunity in a CBG structured around them or not.

Contents

- 1 Why CBG Deserves Serious Startup Attention Right Now

- 2 These are not pilot numbers. This is industrial-scale momentum.

- 3 Government Policy: What’s Actually on the Table

- 3.1 Paddy Straw-Based CBG Plant (Tier-2 Agrarian Belts)

- 3.2 Get Detailed Project Report (DPR): Industrial Biotechnology: Enzymes, Biofertilizers and Biogas

- 3.3 Municipal Solid Waste (MSW) Based CBG Plant

- 3.4 Bio-LNG Production Unit for Export (Joint Venture Model)

- 3.5 CBG-Based Bio-Fertilizer Manufacturing

- 3.6 Related Article: Compressed Bio Gas (CBG) Units: Profitable Green Energy Startup Opportunity

- 4 Import–Export Opportunity Analysis

- 5 Feasibility Planning and DPR Development

- 6 Conclusion

- 7 Data Table: CBG Sector Snapshot for Startup Decision-Making

- 8 FAQ Section

Why CBG Deserves Serious Startup Attention Right Now

The Domestic Foundation Is Being Laid at Speed

By March 31st, 2025, the number of CBG and biogas plants commissioned in India is 100 and the total production capacity is around 700 MT per day. India has 100 CBG and biogas plants with an installed capacity of around 700 MT per day as on March 31st, 2025. Around 336 retail outlets have started the sale of CBG. Indian Oil has commissioned 44 plants and sold about 8.9 thousand metric tons of CBG so far under the SATAT initiative and has 714 active Letters of Intent.

Get Detailed Insights from This Book: Biogas Applications Handbook

These are not pilot numbers. This is industrial-scale momentum.

The CBG Blending Obligation (CBO) framework stipulates that 1% CBG blending is required in total CNG/PNG consumption in FY 2025-26 and the target will be increased to 3% in FY 2026-27, 4% in FY 2027-28 and 5% from FY 2028-29 onwards. This is a form of domestic offtake that is guaranteed by law, and that’s what export-grade production needs as a financial backstop.

The Export Logic Is Simple but Compelling

There are also strong importers of green gas in Europe, Japan, South Korea and some Asian states in Southeast Asia. Germany has been a big producer of bioenergy in the form of biogas in Germany, but feedstock restrictions are slowing the growth. The cost of the LNG imports to Japan is in the tens of billions of dollars per year and the substitution of green gas is a national priority. With year-on-year biomass availability, different agriculture waste streams and now a policy supported CBG sector, India is well poised to take a bow.

The compressed biogas export India opportunity is not about sending CBG in cylinders, the freight economics do not work at the current scale. The real export model is the conversion of CBG to liquefied biomethane (bio-LNG) in ISO containers and with the use of conventional LNG infrastructure. Bio-LNG is already being purchased in Europe for long-term contracts. Structural cost advantage on paddy price lies with Indian producers with access to near zero-cost feedstocks like paddy straw, press mud, and municipal waste, versus the European producers.

Government Policy: What’s Actually on the Table

More comprehensive than most sector founders realize, the Ministry of Petroleum and Natural Gas has developed an architecture of support. Several high-value enablers are confirmed by data from the Annual Report 2024-25 of the Ministry of Petroleum and Natural Gas, Government of India.

The SATAT scheme offers a structure for Oil and Gas Marketing Companies to access CBG from private entrepreneurs through the bidding process under the EoI, thereby eliminating the above-mentioned major risk for the first-time CBG plant owner – the off-take question.

In addition to procurement guarantees, the policy stack comprises central financial assistance under the National Bio Energy Programme of MNRE, classification of the sector as priority sector by the RBI, exemption from excise duty on payment of GST on CBG blended in CNG, development of pipeline infrastructure scheme for CBG injection into CGD network, and market development assistance of ₹1,500 per MT on Fermented Organic Manure produced as by-product. The subsidy for biomass aggregation machinery, which is applicable till FY 2026-27, tackles the biggest operational challenge for rural CBG units i.e., logistics of collecting biomass.

Project Opportunities for Entrepreneurs

-

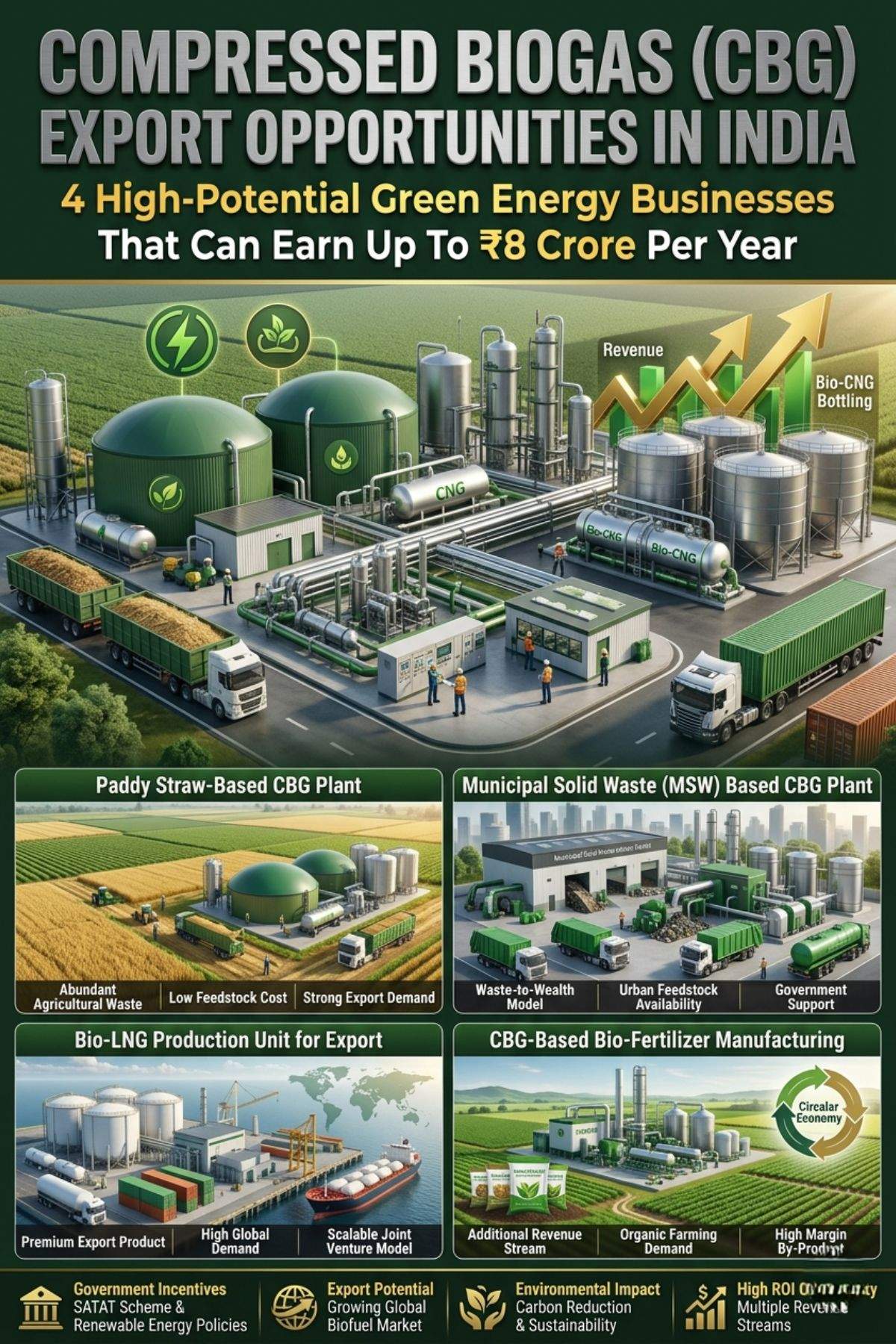

Paddy Straw-Based CBG Plant (Tier-2 Agrarian Belts)

The paddy straw is burnt in millions of tonnes in Punjab, Haryana and in western UP during rabi season. The capex for a 15 – 20 TPD CBG plant based on paddy straw ranges from ₹15 – 22 crores depending on the technology of anaerobic digestion. The gross margins could be as high as 28-34% in case of full utilization at the current OMC procurement price of ₹46-54 / kg along with FOM as a revenue co-stream. The current SATAT LOI are offered to Target Buyers like Indian Oil, BPCL and the HPCL. If the biomass is aggregated from day one in contract, then the scalability path is from 15 TPD to 50 TPD within 3 years. Capital recovery: 6-8 years on equity-based structure, 4-5 years with support from MNRE grant.

Get Detailed Project Report (DPR): Industrial Biotechnology: Enzymes, Biofertilizers and Biogas

-

Municipal Solid Waste (MSW) Based CBG Plant

Wet waste is a problem for urban local bodies in Tier-2 cities due to Swachh Bharat Mission. This is a place that should be attractive to entrepreneurs who can obtain a long-term concession contract from a municipal corporation. The capex needed for the MSW based CBG plants of 5–10 TPD is ₹8–14 crore. Central assistance, apart from the MSW, is offered by the Ministry of Housing and Urban Affairs, which significantly enhances returns for CBG projects. EBITDA margin profile: 22–28% with tipping fees from the municipality factored in to the concession structure.

-

Bio-LNG Production Unit for Export (Joint Venture Model)

This is the most expensive and most profitable. Additional infrastructure cost of bio-LNG unit attached to a 50 TPD CBG plant comes to ₹12–18 crore. Total project cost: ₹35–50 crore. Under green gas certification frameworks, the price of bio-LNG in Europe ranges from €110–150 per MWh, which represents a substantial premium over the domestic CGD offtake price. Requires partnership with green gas registry (ISCC or RedCert2), ISO tank shipping partner and Sale and Purchase Agreement with a foreign buyer. It is the most practical entry structure for Indian MSMEs to join the European companies in a joint venture for diversifying supply chains.

-

CBG-Based Bio-Fertilizer Manufacturing

Each CBG plant will generate digestate as a by-product. Marketing it as saleable bio-fertilizer is an underdeveloped revenue opportunity. The 1,500 per MT on FOM will boost gross margins. An FOM processing unit located with a CBG plant has a Capex requirement of 1.5-3 crore additionally. Customers for bio-fertilizers include organic aggregators, state agricultural departments, D2F etc. Margins on processed bio-fertilizer can go up to 35-40% thereby creating the most margin accretive sub-segment in CBG value chain.

Indian Entrepreneur Case References

Manas Agro Industries (Promoter: Krishna Kumar Gupta) has already a good experience in processing the CBG and bio-CNG projects in Uttar Pradesh with paddy straw as a feedstock. Their model demonstrates that when farmers-producer organizations contract the rural biomass aggregation, the volatility of raw material cost is significantly decreased. The main take-away: do not attempt to own the biomass supply chain, but join it.

Suhas Baxi, the promoter of GPS Renewables Private Limited, has emerged as one of the more systematic companies that are involved in the engineering of biogas plants in India. BPCL has announced a partnership with GPS Renewables for development of CBG plants – direct proof that technology partners having proven capability in anaerobic digestion are premium choices in the SATAT supply chain.

Indian Oil’s purchase of Latinity Bioenergy Private Limited as a 100% subsidiary in December 2024 reflects the importance of CBG being considered as a strategic asset by the major energy players. For entrepreneurs, it provides them with a fair M&A pathway which is not present in many green energy sub-sectors.

Related Article: Compressed Bio Gas (CBG) Units: Profitable Green Energy Startup Opportunity

Import–Export Opportunity Analysis

Currently, India consumes about 50.48% of its total natural gas requirements. This, of course, is because any CBG produced at home and consumed domestically can be considered as an import substitution, hence the government’s rhetoric on import substitution for this sector is financially correct, not rhetorical.

The gap and the opening on the export side are that today there is no significant compressed biogas export India trade flow. The category will be determined by first movers who efficiently establish production scale, green gas certificate and foreign buyer relationships in the next 3-5 years. The Southeast Asian markets are taking shape as potential bio-LNG markets: Vietnam, Thailand and the Philippines are all seeing their industrial sectors decarbonize and lack of their own biomass resources.

Feasibility Planning and DPR Development

It is important for founders to have a detailed and comprehensive Techno-Economic Feasibility Report before investing in CBG projects. Niir Project Consultancy Services (NPCS) prepares market-cum-feasibility report for entrepreneurs who are entering into different types of industrial energy sectors including process flow, feedstock assessment, specification of machinery, project financials and profitability analysis under various capacities. Considering that biogas yield per feedstock type varies by 15-20% and that the choice of technology will have a direct impact on 5-year IRR, a well-structured DPR is not an option, but is a prerequisite for getting bank funding and access to government schemes.

Find high-return business ideas based on your budget & ROI

Conclusion

The opportunity for the export of compressed biogas from India is real but only those who view it not as an opportunity to make a profit on policy but as a manufacturing and logistics problem can take advantage of it. The government has done its bit: obligations are being blended, pipeline infrastructure is being funded, OMC procurement systems are engaged and the biomass subsidy window is open till FY 2026-27.

The sector still lacks entrepreneurs who have an understanding of the economics of anaerobic digestion, can negotiate long-term biomass supply contracts and have the willingness to construct the quality accreditation chain needed to trade biomass internationally. ISCC or RedCert2 certification requires 6–12 months and the charge for each unit is around ₹15 – 25 lakh, which falls between the domestic and export premium price.

HPCL commissioned 484 MT to 3,342 MT of CBG to India’s CBG capacity in just one year, which is a starting point. The blending obligation framework provides a minimum demand of thousands of tonnes per year over the coming decade.

The math is simple when you are a farmer from the MSME community, with access to a geography that is rich in feed stocks, for example the paddy belts in Punjab, the cattle country in Rajasthan, the press mud belts in Maharashtra. Capital is manageable. Policy support is agreed. Domestic offtake is compulsory. For those who build for it, export premium is significant.

The window of opportunity is now open for being the first-mover for compressed biogas export from India. It won’t be open for long.

Data Table: CBG Sector Snapshot for Startup Decision-Making

| Parameter | Current Status / Figure |

| Total Commissioned CBG/Biogas Plants (India) | 100 plants, ~700 MT/day capacity |

| Active SATAT LOIs (IndianOil alone) | 714 LOIs as of March 2025 |

| CBG Retail Outlets Operational | ~336 outlets across India |

| CBG Blending Obligation (FY 2025-26) | 1% of CNG/PNG consumption (mandatory) |

| CBG Blending Obligation (from FY 2028-29) | 5% of CNG/PNG consumption (ongoing) |

| CBG Sale in CGD Synchronization Scheme | Active in 54 Geographical Areas (GAs) |

| HPCL CBG Sales Growth (single year) | 590% increase — 484 MT to 3,342 MT |

| Indicative Capex Range (15–20 TPD plant) | ₹15–22 crore (paddy straw based) |

| Biomass Machinery Subsidy Window | FY 2023-24 to FY 2026-27 |

| FOM Incentive (by-product revenue) | ₹1,500 per MT of Fermented Organic Manure |

FAQ Section

Q1. How much is the minimum amount of capital needed to establish a CBG plant qualified for SATAT offtake?

The capex for a plant with an installed capacity of 2–5 TPD of CBG is in the range of ₹4–8 crore, subject to various parameters like feedstock type, anaerobic digestion technology, etc. If the income from the tipping fees is built into the project, the MSW-based units can range in price from ₹3 to 5 crore in the lower end of the spectrum. The equity outlay can be reduced by 20-30% due to the availability of grant from MNRE.

Q2. How can a first-time entrepreneur get offtake from OMCs under SATAT?

Write an Expression of Interest (EOI) for IndianOil, BPCL or HPCL from time to time. OMC provides a Letter of Intent (LOI) after the site inspection and verification of feedstock. Once the plant is commissioned and quality certified, the LOI will turn into a formal offtake agreement.

Q3. What are the actual hazards in a CBG project which is not fully captured in feasibility reports?

The main risk is feedstock consistency and the yield of biogas changes by 15-20% depending on the moisture content and mix of feedstocks. Small plant interconnection with CGD is not a priority issue. Do not expect 12 months between financial closure and first commercial sale, ensure a minimum of 18 months.

Q4. Whether CBG export from India is viable in the present scenario or still in a speculative context?

At a small scale it is speculative and 50+ TPD with bio-LNG conversion is viable. The economics works when the foreign buyer SPA is signed prior to commissioning and green gas certification (ISCC or RedCert2) is put in place from the start of the project. Not a 3 to 5 year time frame play, but a longer-term play.

Q5. What licenses and approvals are needed to set up a CBG plant in India?

The key clearances that are required are: Consent to establish from State Pollution Control Board, Registration with MNRE for grant eligibility, PNGRB alignment in case of injection pipeline in CGD pipeline, Fire NOC and land use conversion clearance if the land is agricultural. FSSAI registration will be applicable only when digestate is being marketed directly to the farmers as a soil amendment.