LLIN Manufacturing Plant in India

Malaria is by no means solved in India. The country has an unusually high burden of malaria in the South-East Asia Region of the WHO and vector control is the least expensive of the public health arsenal. Mosquito nets that are treated to kill or repel mosquitoes for up to three to five years are known as Long Lasting Insecticidal Nets (LLINs) and they are recommended by the WHO. For a long period of time, India has relied on imports for supplying institutional demand of the Ministry of Health and Family Welfare, state health departments, defence forces, and para-military forces. Now that that dependency is about to split open a realistic domestic manufacturing opportunity. The introduction of HIL (India) Limited in the LLIN manufacturing, where they have developed one product named as HILNET at their Rasayani plant in Maharashtra, is a positive sign for private participation in this sector. The initial capacity already in place is 10 million nets a year. Now, the Indian entrepreneurs have only one question to answer: will they be moving before the import window is closed?

Contents

- 1 Why This Sector Is a Strong Startup Opportunity

- 2 Business Selection Logic and Margin Structure

- 3 Product and Project Opportunities Under the LLIN Sector

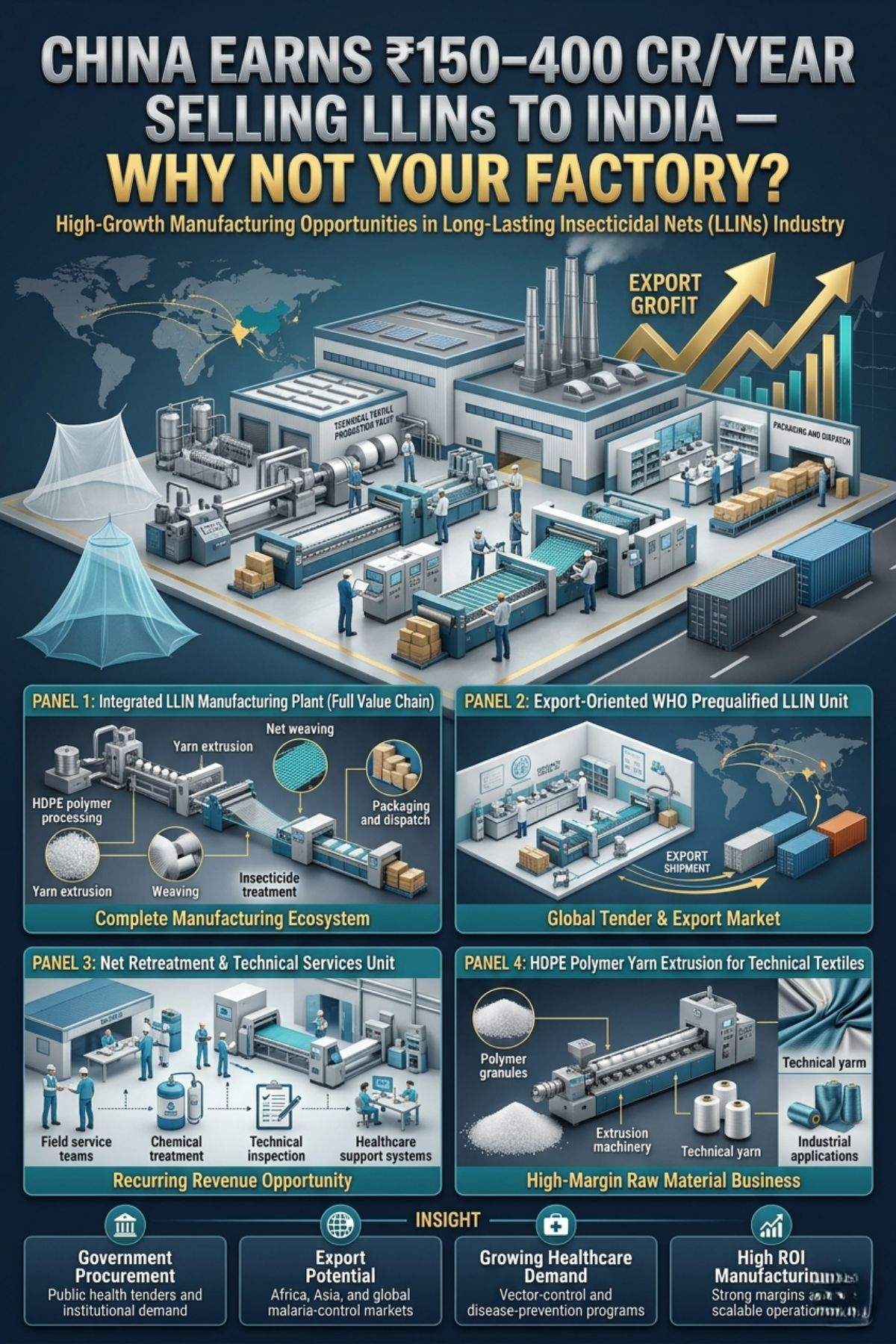

- 3.1 1. Integrated LLIN Manufacturing Plant (Full Value Chain)

- 3.2 Get Detailed Insights from This Book: Woollen Spinning, Weaving, Knitting, Dyeing, Bleaching and Printing Technology Handbook

- 3.3 2. Export-Oriented WHO Prequalified LLIN Unit

- 3.4 3. Net Retreatment and Technical Services Unit

- 3.5 4. HDPE Polymer Yarn Extrusion for Technical Textiles

- 3.6 Get Detailed Project Report (DPR): Technical Textiles: Applications and Project Areas

- 4 Indian Entrepreneur Case References

- 5 Import-Export Opportunity Analysis

- 6 India LLIN Trade Context

- 7 Feasibility Planning: From Concept to Bankable DPR

- 8 Conclusion: A Window of Opportunity-but it won’t remain open for long

- 9 Frequently Asked Questions

Why This Sector Is a Strong Startup Opportunity

Demand signal is clear and institutionalized. The Ministry of Health and Family Welfare (MoHFW) is the buyer of LLINs under the National Vector Borne Disease Control Programme (NVDCP), and the demand for LLINs has been estimated to be at the rate of tens of millions of nets per year. There is also a contribution from the Central Armed Police Forces (CAPFs), defence establishments and NGO distribution chains. Historically all this procurement has been done through imports from countries such as Thailand, China, Sri Lanka etc which make India vulnerable to price volatility and supply disruptions.

This has left the government with a proactive drive to develop locally manufactured options. In the Annual Report 2025-26 of Ministry of Chemicals and Fertilizers, Government of India, Limited developed and commercialized LLINs with a motive to minimize dependence on imports and contribute to the Atmanirbhar Bharat programme. The report further states that the following agencies are being supplied: Ministry of Health and Family Welfare, state health departments, defence forces, CAPFs, PSUs and NGOs — which means that any private LLIN manufacturing company in India would be their direct target.

Investment-wise, this is a sector that has proven institutional buyers, provable import substitution rationale and policy support. It is unusual to find that combination. For the majority of manufacturing startups, it’s an imperative that they build demand. LLIN entrepreneurs can enter into an already established, funded demand curve.

However, there are real entry barriers that are not prohibitive. An Indian LLIN manufacturing plant which includes the polyethylene monofilament extrusion line, net-weaving machine, insecticide treatment line, and quality testing facilities generally requires an investment of Rs. in the project. 8 crores to Rs. The cost, depending on size and automation, is 25 crores. The licensing requirements are that it must be registered with the Central Insecticide Board and Registration Committee (CIB&RC) and meet the WHO standards (PES 60 denier standard). High density polyethylene (HDPE) granules, LLDPE granules and alpha-cypermethrin / deltamethrin active ingredients are all available domestically as raw materials.

The government scheme support is available via PMEGP (small units up to Rs. 20 lakh project cost under manufacturing, CGTMSE collateral free facilities for MSMEs and potential PLI benefits to LLIN nets in specialty textile and technical textile categories.

Related Article: India vs China Manufacturing: Best Business Opportunities, High Profit Sectors & Startup Ideas in India

Business Selection Logic and Margin Structure

There are two decisions involved in the profitability of LLIN manufacturing: product specification and buyer segmentation. WHO-prequalified LLINs cost more in institutional procurement, and have a higher level of investment in testing, documentation and compliance. Non-pre-qualified nets for domestic level buyers of MSMEs or government schemes of sub-national level are characterized by lower entry cost, but are subjected to margin pressure.

A mid-scale LLIN manufacturing plant, capable of producing 2-3 million LLINs per annum, can have an EBITDA margin of 18-24% with institutional supply contracts. Polymer granules, which account for approximately 35-40 percent of cost of goods sold, and insecticide active ingredients, which account for approximately 12-15 percent, are the two most significant cost drivers, as is energy. The cost of labour is significantly lower in Tier-2 manufacturing hubs such as Nagpur, Nashik and Aurangabad compared to metros.

Modular investment in extrusion lines is required to achieve scalability from a pilot unit of 500,000 nets per year to a medium size unit of 5 million nets. The capital equipment used is mostly conventional, adapted to technical requirements — not fancy. The learning curve will be manageable to technical textile promoters, agri- nets promoters, and shade nets promoters.

Here, being aware of the danger is important. The regulatory risk is the most acute one: WHO prequalification is not a straightforward process, and CIB&RC registration requires time. The risk that comes from the government’s demand side is that the number of tenders or the volume of demand for a year may change. Raw material risk, particularly in the case of insecticide active ingredients, can be addressed, to a certain extent, by contract manufacturing agreements or in-house blending. However, those entrepreneurs, who establish direct relationships with the NHM procurement officers, instead of depending on the open tenders, get much better capacity utilisation.

LLIN Manufacturing: Project Opportunity Matrix

| Project Type | Production Scale | Target Buyer | Capex Range | Margin Outlook |

| LLIN Net Weaving Unit (Pilot) | 0.5–1 million nets/annum | State health depts, NGOs | Rs. 4–8 Cr | 12–16% |

| Integrated LLIN Plant (Mid-Scale) | 2–5 million nets/annum | MoHFW, CAPFs,

Defence |

Rs. 10–20 Cr | 18–24% |

| WHO Prequalified Export Unit | 5–10 million nets/annum | Africa via WHO/UNICEF

tenders |

Rs. 20–35 Cr | 22–28% |

| Net Finishing & Treatment Hub | 2–3 million retreated nets | MoHFW, state depts | Rs. 3–6 Cr | 14–18% |

| Polymer Yarn Extrusion (Upstream) | 500–1,000 MT

yarn/annum |

LLIN manufacturers | Rs. 6–12 Cr | 16–20% |

Product and Project Opportunities Under the LLIN Sector

1. Integrated LLIN Manufacturing Plant (Full Value Chain)

This is the opportunity that is needed the most. An LLIN manufacturing setup consists of one plant that has an in-house HDPE monofilament extrusion line, Raschel knitting or warp knitting machines for the production of net fabric, and an insecticide treatment bath. Institutional tenders for commercial scale production, in India, are in the range of 3 to 5 million nets per year. The target buyers are procurement division of MoHFW, state National Health Missions and defence procurement agencies. Capital expenditure comes under Rs. 12 crores and Rs. This combination will cost 20 crore rupees. EBITDA margin outlook, at stable institutional supply, is at 18-22 percent with working capital as the key cash-flow driver, linked to tender cycles.

Get Detailed Insights from This Book: Woollen Spinning, Weaving, Knitting, Dyeing, Bleaching and Printing Technology Handbook

2. Export-Oriented WHO Prequalified LLIN Unit

The global LLIN market is a multi-billion-dollar procurement channel, fuelled by the demand of sub-Saharan Africa, and financed by Global Fund, UNICEF and PMI (US President’s Malaria Initiative). This is the opportunity that WHO prequalification provides. Indian businessmen who are patient enough to go through the process of prequalification for 24 to 36 months can aim for export business worth Rs. 50 crores to Rs. An additional 150 crore per annum at higher margins than domestic. The cost of capital rises to Rs. An investment of Rs 25 to 35 crores for compliance of WHO’s strict quality and process documentation. The lesson learnt from HIL’s HILNET development is that technical cooperation with CIPET or research institutes is more important than in the domestic institutional market, where the polymer science expertise provided by CIPET was indispensable.

3. Net Retreatment and Technical Services Unit

LLINs become ineffective after 3-5 years and must be re-treated using one of the approved insecticides. A retreatment services unit for state NHM LLIN fleet is a relatively low capex entry point (Rs. The company expects to generate recurring, sticky revenue of 3 to 6 crore. The model is best suited to be implemented as an MSME operation in malaria endemic states of the country such as Odisha, Jharkhand, Chhattisgarh, Madhya Pradesh, and northeastern states. Application of insecticide is under the CIB&RC licensing regime. Margins are lower than manufacturing at 14-18 percent EBITDA but capital efficiency is good.

4. HDPE Polymer Yarn Extrusion for Technical Textiles

There is a lack of players filling in the gap of upstream yarn supply in Indian LLIN value chain. The fine denier extrusion unit is capable of extruding 60 to 150 denier HDPE monofilament suitable for LLIN manufacturers and other agri-net, shade net and geotextile applications. This spread of the customer base significantly lowers the risk of demand concentration. The cost of the project is Rs. The yarn business of 500 to 1000 MT per annum would run with 6 to 12 crore. Quality control can achieve margins of 16-20%.

Get Detailed Project Report (DPR): Technical Textiles: Applications and Project Areas

Indian Entrepreneur Case References

Direct lessons for those who think of the LLIN manufacturing space in India from three industrial promoters.

V.K. Chaudhary, Managing Director of Garware Technical Fibres Ltd. (formerly Garware-Wall Ropes), systematically pitched his products, which were import-substitute and quality to international standards, to institutional buyers such as fisheries, aquaculture, sports, and succeeded in establishing one of the largest technical textile businesses in India. His strategies of investment in R&D, seeking international certification and establishing long-term supply partnerships with government bodies are directly transferable to the LLIN sector. The lesson: Credibility within institutions takes 3 to 5 years to establish and lasts long after that.

With an eye on Government schemes and agricultural institutions, technical agri-net and shade net manufacturers Arvind Sinha of Centrotex Group and Brijlal Obhan & Sons had carved a niche before they branched into exports. The approach of scaling up from domestic institutional supply, stabilize cash flows and then progressively seek WHO or export grade improvements is the risk management strategy right for LLIN entrepreneurs with no prior experience in medical grade textiles.

The product development journey of HIL (India) Limited, in the direction of its CMD under the technology partnership with CIPET and sourcing of raw materials from within the country to minimize the cost and logistics risk, along with the positioning of the product specifically as a ‘Atmanirbhar Bharat’ is a reflection of the fact that the journey of the product development is not a guessing game. Private promoters can sign similar technology collaboration agreements with CIPET’s 48 centres located across India, and IPFT’s formulation expertise to get a considerable relief from R&D.

Import-Export Opportunity Analysis

India now has a significant institutional demand for LLINs which is not met locally. China is the major source in polyester nets, Thailand and Sri Lanka. The prices of imports have varied from Rs. 150 crore and Rs. In high procurement years, 400 crore is spent per annum, subject to the extent of the rollouts of WHO-funded programmes. This import flow will be the first one to be displaced in an LLIN manufacturing plant in India.

The global LLIN market is estimated to be more than USD 800 million per year; more than 85 percent of the volume is estimated to be in the sub-Saharan Africa region on the export side. India’s competitive labour cost, a good polymer manufacturing base and technical capability due to WHO prequalification makes it look like India is competitive with Chinese and Europeans, especially its proximity to East African ports. Indian manufacturers with the status as WHO-prequalified can tap into the tender cycles of the Global Fund and UNICEF, which run into hundreds of millions of dollars every year.

India LLIN Trade Context

| Parameter | Current Status | Opportunity | Key Markets |

| Domestic LLIN import dependency | High — majority imported | Full import substitution possible | China, Thailand, Sri Lanka |

| Domestic institutional demand | ~10–20 mn nets/annum (estimated) | Rising with NHM allocations | MoHFW, State NHMs, CAPFs |

| Global LLIN market size | USD 800 mn+

annually |

Export via WHO prequalification | Sub-Saharan Africa, SEA |

| Export potential for Indian LLIN plant | Nascent — HIL pioneering | Rs. 50–150 Cr export contracts | Global Fund, UNICEF tenders |

Feasibility Planning: From Concept to Bankable DPR

Any serious promoter should have a detailed techno-economic analysis before investing in any manufacturing project for LLINs. Niir Project Consultancy Services (NPCS) prepares detailed Market Survey cum Techno-Economic Feasibility Reports for entrepreneurs wanting to establish manufacturing units in a variety of sectors like technical textiles and public health products. These reports include all the data an project evaluator would require: manufacturing processes documentation, production volume mix and capacity planning (assumptions), machine information and vendor comparison, raw material sourcing information, and full financial information including break-even analysis, IRR and profitability over a 7–10-year period. A well-structured DPR is not an option for LLIN manufacturing, which is subject to the added regulatory complexity of compliances with the requirements of CIB&RC licensing and WHO specification. It is the document which makes or mares a term loan for a bank.

Find high-return business ideas based on your budget & ROI

Conclusion: A Window of Opportunity-but it won’t remain open for long

India is in a unique space with its LLIN manufacturing industry – a combination of assured demand from institutions, enthusiastic government support for import substitution, a PSU that already demonstrated the technical viability and an export market waiting for certified quality manufacturers. The HIL-CIPET partnership which delivered HILNET established the fact that the product can be manufactured in India, with indigenously sourced raw materials. That proof of concept considerably reduces the risks for the private entrepreneur who steps into the market.

The expected range of capex required for a small- to medium-scale LLIN manufacturing facility in India to be commercially viable is estimated to be betweenRs.10 crore and Rs. 20 crores. The required funds could come from the promoter’s equity, a term loan under the CGTMSE collateral-free guarantee scheme, and potential incentives provided for MSME clusters. A break-even in 24–30 months’ time for a plant focused on institutional supply contracts is achievable at 60–65% capacity utilization.

There are three critical factors which define success in this sector-the speed of registration by the CIB&RC and obtaining WHO prequalification (start the process now), the establishment of deep relationships with institutional buyers (begin relationship building early with the MoHFW and State NHMs) and security of raw material supplies (back-integrate to produce yarn, or contract with HDPE processors, ideally in Gujarat and Maharashtra, to source your inputs).

This window will not remain open for long. As capacity starts to build – the first of the Bit bio- larvicide facility is being set up at HIL’s Rasayani facility – it will begin to erode the advantages enjoyed by first movers in private LLIN manufacturing. Entrepreneurs who step in during the next 18–24 months, armed with considerable capital and a strong institutional buyer strategy, stand to gain a much greater benefit from the business than those who decide to wait.

Frequently Asked Questions

Q1. What is the minimum investment required to set up an LLIN manufacturing plant in India?

The cost of establishing a pilot-scale plant that manufactures 500,000 to 1 million nets annually is estimated between Rs. 4 to Rs. 8 crore which includes extrusion machinery, knitting machines, treatment plant and basic testing equipment. A commercially optimum medium scale unit that produces 3 to 5 million nets annually can be set up for Rs. 12 to Rs. 20 crores. Smaller scale plants may receive funding up to some part from CGTMSE guarantee and PMEGP.

Q2. What licenses and registrations are mandatory before production?

Registration from Central Insecticide Board and Registration committee (CIB & RC) must be acquired for the insecticide treatment aspect of the LLIN. The specification from WHO (Pesticide Evaluation Scheme – PES standard) is a must for institutional government supply. A separate WHO pre-qualification is to be obtained to participate in global tender. BIS quality mark under Deptt. Of Chemicals & Petrochemicals might be applicable for the polymer raw material for manufacturing.

Q3. What is the break-even timeline for an LLIN manufacturing unit?

At 60 to 65 percent capacity utilisation with institutional supply contracts in place, a mid-scale LLIN plant can break even within 24 to 30 months of commercial production. The critical variable is the procurement cycle: MoHFW and state NHM tenders are periodic, so working capital management during inter-tender gaps significantly affects the actual break-even trajectory.

Q4. Can Indian LLIN manufacturers compete in global export markets?

Yes – only if Whopper-qualified. India has competitive advantages of lower conversion costs, supply of domestic HDPE polymer from Gujarat and Maharashtra and CIPET aided technical quality assurances. The main buyer segments are Global Fund, UNICEF Supply Division and bilateral aid programmer mainly directed to sub-Saharan countries. Prequalification normally takes 24 to 36 months and requires very good product documentation.

Q5. What are the key risks an investor must account for before entering LLIN manufacturing?

Key three risks: (1) Regulatory risks (timelines for licensing approval from CIB&RC, WHO approval); (2) Demand concentration risks (reliance on one state for NHM purchasing); (3) Price fluctuation of active insecticide ingredients. Minimize by applying for and acquiring licenses early in two tracks concurrently; diversified customers with minimum of three buyers including