Hidden Charges in MSME Bank Loans

The Loan You Got Is Not the Loan You Signed Up For

As part of the process, thousands of MSME entrepreneurs in India each year look into business concepts, secure fundings and approach banks for borrowing, only to realize months later that the amount they had to pay for the loan was far more than the interest rate quoted. Sanction letters with embedded processing fees. Embedded processing fees in sanction letters. Buried in a 40-page agreement, clause 18 contained pre-payment penalties. No single conversation required for insurance premiums to be bundled. These are not simple errors. They are the inherent characteristics of business lending in India — and not many MSME founders can identify them.

It’s not just a financial disaster. It is informational. When a small manufacturing or trading business is run by a first-generation entrepreneur, it is highly unlikely that he/she will have a CFO to read the loan papers line by line. They are going to trust the relationship manager. What the relationship manager will likely not mention is the true cost of a loan — post all the fine print.

The Reserve Bank of India (RBI) mandates banks to show the Annual Percentage Rate (APR) of loans (which includes all charges). But there is limited adherence to this disclosure standard, and even the majority of borrowers are not educated on how to read and understand APR data. It leads to a systematic mismatch between what MSMEs believe they’re paying, and what they actually are.

Why MSME Borrowing Is a High-Stakes Game

MSME is the backbone of India’s economy. The Ministry of Micro, Small and Medium Enterprises estimates that it contributes almost 30% of the GDP and employs more than 11 crore people. The demand for credit in the sector is enormous – and expanding. However, the average MSME borrower is still not well educated financially, and is especially sensitive to the types of loans that yield the highest profits for the lender.

Consider the math. A manufacturing MSME takes loan of ₹50 lakh at a nominal interest rate of 11% per annum. The interest that has to be paid annually is ₹5.5 lakh on paper. However, once you factor in the processing fee (1.5%), the bundled insurance (1.2% per annum), documentation charges (₹15,000) and penal interest incurred during a cash crunch of two months, the annual cost is easily more than 16% to 18%. That’s a huge amount. And it eats into the razor-thin profit margins most MSMEs have.

Thus, it’s not a financial literacy exercise to just understand these hidden charges. It’s a must learn skill for every MSME founder in the competitive environments of today.

Related Article: DPR for Bank Loan: Format, Example & Step-by-Step Guide for MSME Loan Approval

What the Regulatory Framework Says — And Where It Falls Short

The RBI’s Fair Practices Code for Lenders says that banks and NBFCs must clearly and simply write down all charges related to their loan in the first place. Further, the MSME Samadhaan platform enables MSMEs to lodge any complaints related to payment. But disclosures of pre-disbursement charges are not enforced very well.

There has been some progress made by the government. Pradhan Mantri Mudra Yojana (PMMY) is an initiative by the government to provide collateral-free loans. There are three schemes namely Shishu, Kishore, and Tarun with comparatively transparent fee structures. The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme minimizes the requirement for collateral and to a certain degree, insurance bundling. But, none of these schemes has gone to the extent of resolving the issue of undisclosed charges in conventional term loans and working capital facilities provided by the commercial banks.

It is also worth noting that the DPIIT has created a Startup India portal with grievance redressal and financial advisory tools for the benefit of the startup entrepreneurs to help them better understand lender disclosures. Furthermore, the Federation of Indian Chambers of Commerce and Industry (FICCI) has been highlighting hidden lending charges as a structural impediment in expanding the MSME growth in India.

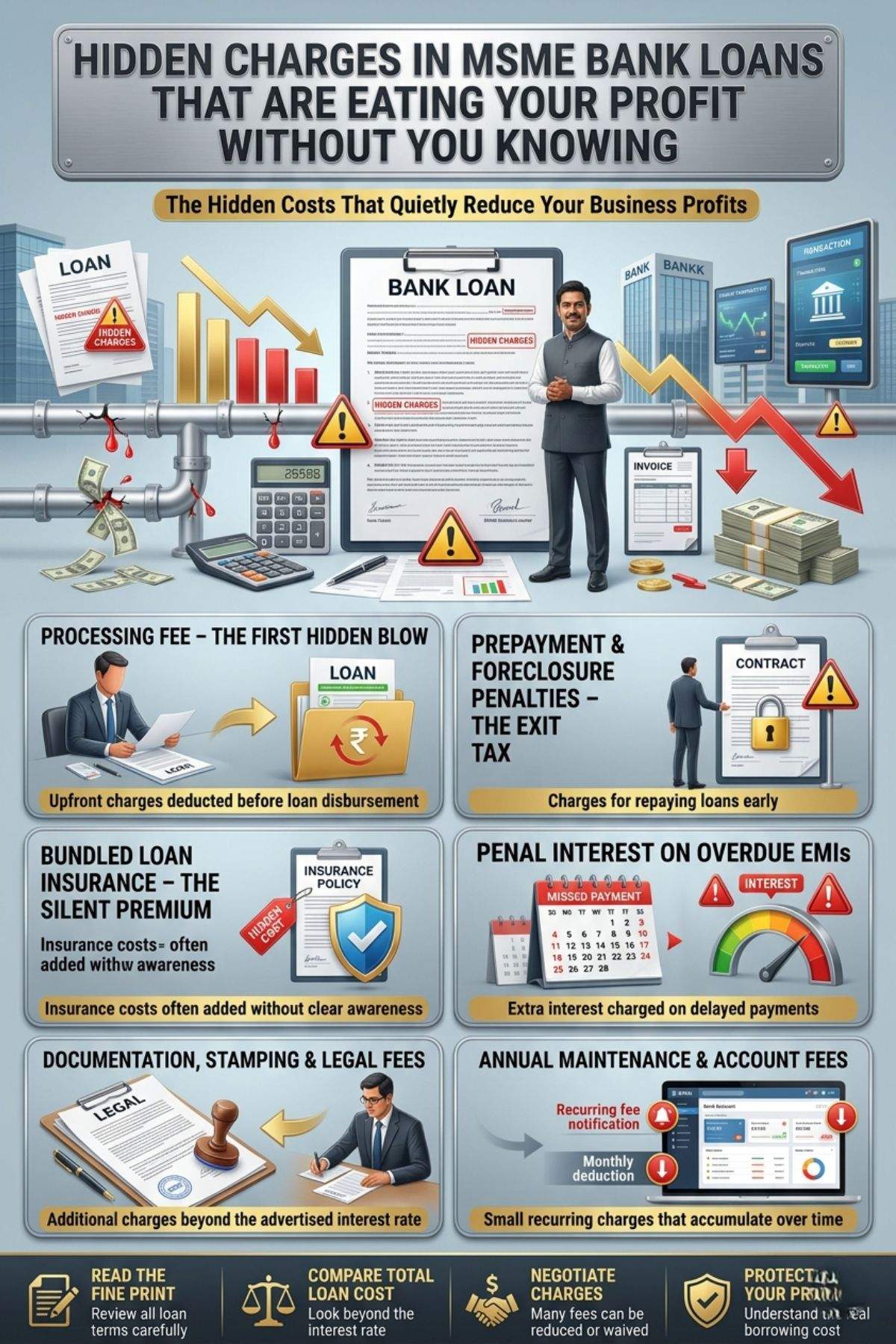

The Major Hidden Charges That Are Costing MSMEs Dearly

1. Processing Fee: The First Hidden Blow

Most founders know of the processing fee, but very few realize just how big it can be. This fee will be deducted from the sanctioned loan amount and is generally 0.5% to 2% of the sanctioned amount. If you apply for a loan of ₹50 lakh, and the processing fee is 1.5%, you’ll receive ₹49.25 lakh, but you’ll be charged interest on the entire amount of ₹50 lakh. It’s a structural feature that results in your effective interest rate starting higher than what it purports to be on the first day.

3. Prepayment and Foreclosure Penalties: The Exit Tax

This is where most of the MSMEs really get taken aback. During a boom time, once the business gets better and cash flows are available, the natural inclination is to settle the loan before the time, which helps in reducing interest payments. But a lot of bank loans are subject to prepayment penalties of anything from 2 per cent to 4 per cent of the outstanding principal. A few lenders may have a lock-in requirement of 12 to 24 months, meaning you can’t make a single payment at all. This is effectively locking a borrower in to a high-cost loan when they are able to pay it off. This means that the actual price of borrowing is more expensive than any apparent interest rate comparison might indicate.

Your investment deserves the right opportunity

3. Bundled Loan Insurance: The Silent Premium

This is probably the most obscure of all the hidden fees. Credit life insurance or loan protection insurance is offered by many banks, especially public sector banks, as a part of the loan disbursement process. This is the premium which is levied on the loan at the rate of 0.5% to 1.5% per annum either as a lump sum or as an additional payment to the EMI structure. The borrower is not always made clear that the insurance is optional. The Insurance Regulatory and Development Authority of India (IRDAI) has released guidelines that mandate that borrowers be informed of the option of insurance provider, but this is often not done. This causes the hidden cost of ₹5,000 to ₹20,000 a year to a mid-size MSME’s loan.

4. Penal Interest on Overdue EMIs

There will always be cash flow mismatch in the life of MSMEs. EMI payments are often delayed due to various reasons, such as customer payments, seasonality issues, or supply chain disruptions. Penal interest is usually applied on the outstanding balance, at a rate of 2% to 3% per month, by banks. The compounding effect is what makes this punishing. The penal charges alone on a ₹10 lakh EMI can be as high as ₹20,000 to ₹30,000, if the documents are delayed by two months. If the borrower finds that he is getting three or four such delays in a three-year loan period, the total penal interest can add up to several EMI payments.

5. Documentation, Stamping, and Legal Fees

These charges are not discussed – let a long way as not quantified – when you apply for the loan. Documentation charges, charges by advocates in case of verification of property, stamp duty charge on mortgage creation and charges on stamping of loan agreement can vary between ₹5,000 to ₹25,000 or even higher depending on the loan. For a loan amount of ₹25 lakh, this is a one-time cost of up to 0.1%, which may seem negligible on its own, but when combined with all the other hidden costs.

6. Annual Maintenance Charges and Account Fees

There are banks which impose annual maintenance charges for loan accounts, especially for working capital accounts and also for the overdraft limit provided. The charges, from ₹2,000 to ₹10,000 per year, are seldom discussed at the time of sale. Likewise, if a business has cash flow that is not consistent, the business may end up paying ₹500 to ₹1500 per instance of the ECS or cheque dishonour fee. Often these charges are hidden in the loan statement as administrative costs and not easy to see without doing a line-by-line review.

Get Detailed Insights from This Book: 50 Best Home Businesses To Start With Just 50,000

How Hidden Loan Charges Affect Export-Oriented MSMEs Specifically

The risks are even greater for export-oriented MSMEs. Many of these businesses are known to opt for short-term pre-shipment credit loan or packing credit loan, which comes with additional fees and charges over the basic loan rates. The actual cost of borrowing includes currency hedging costs, LC discount costs and export credit insurance premiums.

Besides, export receivables have an unpredictable timing. A delayed Letter of Credit from an overseas buying party may result in penal interest being charged on a domestic loan repayment – a double whammy that is a blow to the export margin. Many MSMEs selling overseas to the Gulf, Africa, or Southeast Asian countries develop the habit of reporting on hidden loan charges, which can account for a whopping 3% to 5% of all export sales, and make a big difference between making a profit and losing money.

Export-Import Bank of India (Exim Bank) has MSME specific export finance products with better fee structures. For export-oriented entrepreneurs, there are various export facilities available with Exim Bank, which are more cost transparent as compared to commercial bank credit lines and should be actively considered.

Indian MSME Leaders Who Learned the Hard Way — and Then Won

Kiran Mazumdar-Shaw, Biocon Limited

Biocon is founded by Kiran Mazumdar-Shaw who grew the company from a small enzyme manufacturing unit in Bengaluru to become one of the largest biopharmaceutical companies in India. When she started her business as an MSME in the late 1970s, she faced difficulty in getting formal bank credit and a lack of understanding about the credit. She has been public about the opaque nature of business lending at the beginning stages – the actual interest rate was not always divulged and monthly cash flow was a basic struggle to survive when repaying high-cost loans. She was eventually successful because of a sensible financial management philosophy – knowing each and every expense in a loan application before committing. So, her lesson to the MSMEs of today is very simple — when it comes to the fees, read every clause, negotiate every fee, and do not assume that what the bank says verbally is what is in the document.

Viveks Retail: The Story of Reading the Fine Print

Viveks is one of the most successful MSME success stories in organised retail in South India. They expanded from being a family business based in Chennai into a multi-city business, primarily with the assistance of trade credit and bank working capital facilities. Their finance team had to learn one of the things early on: the “all in” cost of borrowing—all fees, penalties and insurance costs—before they would compare loan offers from various banks, company insiders said. This simple practice resulted in the company saving many, many dollars in decades and was the standard operating procedure. The takeaway: Make your loan assessment process uniform. Don’t look at just the interest rate.

Manjushree Technopack: Turning Financial Literacy Into Competitive Advantage

Manjushree Technopack, a small plastic packaging unit in Bengaluru has grown into one of the largest rigid packaging manufacturers in India. They went through several cycles of loan financing in the form of terms loans. The firm’s management has discussed its advantage in negotiating with lenders with a comprehensive knowledge of loan covenants, prepayment structures and fees. By the time the firm expanded to a point where they could refinance for lower rates, they had built their very first loans so as they did not get penalized for prepayment. The result was crores saved at exit. One key takeaway from their model is that financial sophistication at the MSME level is not an indulgence. It’s a competitive moat.

Get Detailed Project Report (DPR): Project Reports & Profiles

How Professional Feasibility Support Can Help MSMEs Avoid Financial Traps

Some of the best practices when it comes to MSME financing is to arrive at the lending process having a professionally ready project report and financial model. Some of the best practices when it comes to MSME financing is to be able to bring a professionally ready project report and financial model to the lending process. Once borrowers have given a banker a techno-economic feasibility project that has been well-tuned, and that contains detailed cash flow projections, a break-even analysis, and sensitivity scenarios, the discussion on loan structuring changes. The borrower will no longer be in reactive mode. They can identify the kind of loan, the term and the flexibility of repayments they require.

At Niir Project Consultancy Services (NPCS), we offer professional consultancy for Market Survey cum Detailed Techno-Economic Feasibility Reports (DPRs) for setting up new industries/Businesses. Detailed Manufacturing Process, Market Research and Demand Analysis, Process Flow Diagram, Product Mix and Capacity Planning, Machinery and Material Details, Project Financials, Profitability Analysis and much more are included in our reports. Our goal is to assist entrepreneurs to perform feasibility studies, profitability and long-term scale before investing. An entrepreneur who presents a DPR prepared by NPCS at a bank walk in with data, and walks out with a better loan.

Key Hidden MSME Loan Charges: A Quick Reference Table

The table below summarises the most common hidden charges in MSME bank loans, their typical range, and their practical impact on borrowers.

| Charge Type | Typical Rate / Amount | Disclosure Frequency | Impact on Borrower |

| Processing Fee | 0.5% – 2% of loan amount | Usually disclosed | Upfront cost, reduces net disbursement |

| Prepayment Penalty | 2% – 4% of outstanding principal | Rarely disclosed upfront | Traps borrower in high-interest loans |

| Loan Insurance Premium | 0.5% – 1.5% of loan per annum | Often bundled silently | Adds 10%–20% to total loan cost |

| Documentation / Legal Fees | ₹5,000 – ₹25,000 per case | Inconsistently disclosed | Hidden in miscellaneous charges |

| Penal Interest on Delay | 2% – 3% per month on overdue | Fine print only | Compounds rapidly on cash-flow gaps |

| Annual Maintenance Charge | ₹2,000 – ₹10,000 per year | Rarely disclosed | Erodes working capital over loan tenure |

| Cheque / ECS Bounce Charge | ₹500 – ₹1,500 per instance | Buried in schedule | Punitive during seasonal cash crunches |

Source: Compiled from RBI Fair Practices Code, MSME industry reports, and SIDBI lending guidelines.

Frequently Asked Questions (FAQ)

Q1: Does it legal to banks to pass some charges and does not inform you.

No, it does not legal, according to RBI guidelines the Fair Practices Code stipulates that while sanctioned a loan lender are required to disclose all applicable charges. However, enforceability is often lax. Always ask your bank for a detailed list of charges before you sign. Don’t consider verbal agreements about these fees as factual information.

Q2: Are the prepayment penalties on MSME loans negotiable.

Yes, the banks allow negotiation, the chances are very higher for those that have good credit history or existing banking relationships. Please request the banks for the zero prepayments penalty after 12 months and you will most likely to find banks which agree to the clause. It saves you a significant amount of money especially when your business gets grow at faster than expected.

Q3: Is it compulsory for MSME loans to take the loan insurance?

No, but most of the time the banks add the insurance in the package without proper information of the insurance. The IRDAI guideline allow you the to opt your own insurer for credit life insurance in case the bank ask to add insurance into loan package, please consider asking from the bank a written policy, which states this will be one of the eligibility conditions for sanction of loan or decline if they refuse. Avoid the insurance which is not properly explained with the all-relevant charges and the benefits.

Q4: how to calculate all over cost of MSME loan.

Calculate the Annual Percentage Rate (APR), processing fee, insurance, documentation charges, and any penal interest in case the cash flow doesn’t follow the predicted cashflow pattern as predicted while applying the loan, this would give a roughly effective annual cost. Request the bank for the full loan cost structure – a right of borrower as per RBI guidelines.

Q5: What should be done in case some wrong or hidden charges passed without prior disclosure post disbursement.

Send an email with a written grievance to the grievance officer of the bank, asking them to furnish detailed reason for charging. If not satisfied write to the RBI’s Banking Ombudsman scheme as it is free formal dispute resolution procedure for all bank’s customers, all you need to retain the evidence like email, signed loan papers etc. It’s very surprising how many entrepreneurs suffer with unfair charges only because they are unaware of Banking Ombudsman Scheme.

Q6: Are NBFCs loan more Transparent compare to banks in case of MSME loans?

No NBFC loans aren’t often any more transparent than bank loans for SMEs. In fact, the hidden costs that NBFCs have could possibly exceed what a bank would charge. There has even been criticism levied against some Fintech NBFCs due to the fact that they may not fully reveal the actual annual interest rate the bank is charging. However, same as for banks, you should insist on obtaining full details and schedule of charges before signing. NBFCs still adhere to RBI regulations on fair lending practices, meaning your rights as a borrower aren’t compromised.

Conclusion: The Most Important Line in Your Loan Document Is the One You Almost Skipped

They are not just a nuisance, a hidden charge burden which adds 3-5% to the effective cost of a MSME’s loans (often earned on margins of 8-15%) determines if it has a profit or a loss on an annual basis. The answer is not to shun bank loans – as finance is oxygen for MSME’s growth. The answer is simply too smart loan

Read every clause. Ask every question in writing. Calculate the all-in APR before comparing loan offers. Negotiate prepayment flexibility from day one. Decline insurance products that are not explicitly explained. And if you are preparing a project or entering a new venture, start with a professionally prepared feasibility report that gives you the financial clarity to approach lenders from a position of strength — not desperation.

While sometimes the banks are your allies, understand the simple fact, a bank is a business too – working towards its profitable optimum. As an MSME founder, you’re striving for yours. And to start, understand exactly what the price tag is.